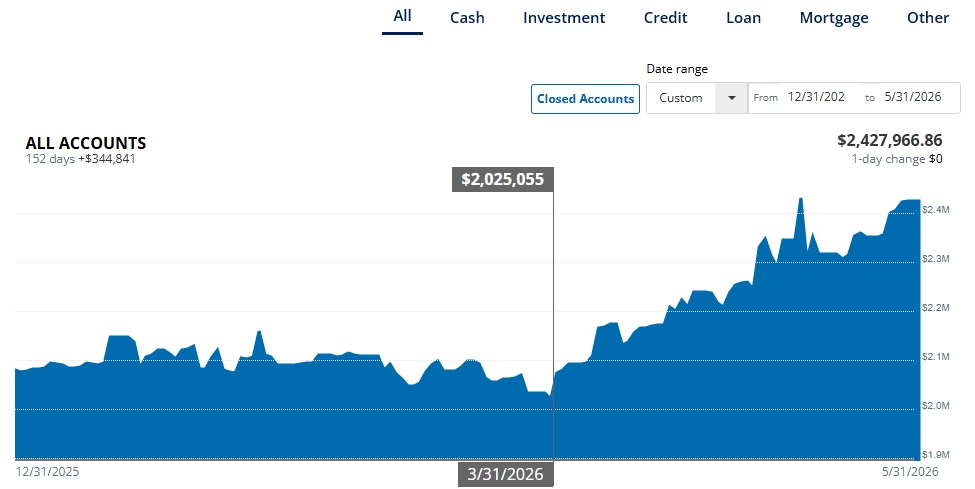

We are up $340k! Best Time to Invest may have been 45 days ago.

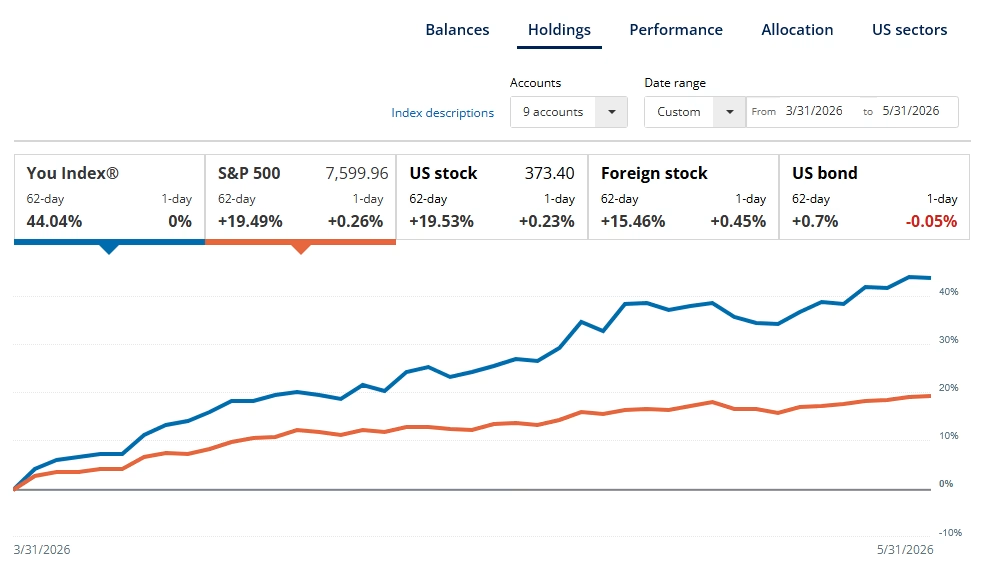

For the fourth time (in a row), May locked in our best investment performance month. The force is indeed strong. The Nasdaq Composite (+8.4%) yanked our portfolio by the neck. Since March 31, the gains have been 24.93 percent. This represents a powerful upward trajectory with even more steam left through July 31. While the bulk of the heavy lifting was done by powerhouses like SNDK (+165%), AMD (+150%), and Nvidia (+20%), retail traders are moving feverishly to recoup losses. Those who bought the dip following the drop on March 30 are eating well. We lucked out since our portfolio leans nearly +50 percent in the technology sector.

Over the last six years, my wife and I tweaked our household’s investment style. This will include selling for profit when possible and learning to let go of losing positions. We’ve become more diligent with at least 10 percent or $175,000 in investment cash reserves. Since we can’t time the market, the next best thing is to have available resources to buy dips. The name of the game is to remain flexible. So far, it’s been working out for us. Our 1-year return is up 101.24 percent versus the S&P at 28.22 percent.

The world’s economy still hinges on the trade deal between China and the US. While the Iran conflict continues to waver, it’s best not to panic. I still believe that interest rate cuts are likely off the table for 2026. Besides being a bumpy year, financial sailing should be choppy but positive. The new Trump era is increasing the K-shaped disparity. As AI adoption surges, make sure that you aren’t missing the human component. Check on your friends and family. Take care of yourself. Health is a strong component of wealth. Get out of the house for some much-needed sunshine and grab some grass. I highly recommend a return to normal.

As for the TNFG family, we were spending as if the sun won’t shine tomorrow. The mid-year trip took us to Mexico City. In May, we spent nearly $2,000 on travel. Now, we are looking forward to Peru + Colombia in the fall. We are still proving that it’s possible to spend and still build wealth. Check it out, how Black families can build generational wealth, according to experts.

Table of Contents

If it’s not Inflation, it’s SMH [ETF]!

In market news, inflation persists. Albeit more muted as prices escalate due to the Iranian conflict. US families are financially fatigued at this point, with gas prices expected to increase for Freedom 250’s summer. Pandemic savings ran out. Debt spending is mounting. We are all feeling the pinch from groceries, shopping, and even casual dining. The Average American is struggling to pay an extra $7,000 in additional expenses per year. The blame fell on immigrants, but in reality, we are spending too much.

When times are tough financially, people blame the rich, and then they blame the politicians. In a master use of word play, the politicians try to blame the rich, but since they are rich themselves, they blame immigrants or people who live off the system. It’s easier to blame immigrants since they are nameless. The true final boss is personal cutbacks, where possible, and an increase in taxes on everyone. Since those solutions aren’t easy and digestible, politicians substitute the colosseum with pseudo tax cuts. This is what the One Big Beautiful Bill is all about. It’s all short-term benefits to kick the can down the road.

Unfortunately, nothing changes unless you change. Americans will face their household’s rolling recession based on the excess lifestyle spending loop. Try not to think of recession as an overall national problem; think of it as an individualized household problem. The more we spend, the worse it will get. Layoffs are one thing; the employment recovery is quite another. There is a growing contingent of younger Americans ending up jobless. Inversely, for investors, times are great.

Inflation, Midterms, and Expensive Date Nights

Intuitive ways to stop losing future opportunities: “Learn to Spend Less.“

Treat the rest of 2026 as if you were in 2020. Invest more in Energy, Utilities, and Consumer Staples, even if the Tech side is surging. Try to buy when quality companies are low.

Pull back where you can and try not to stash money in a savings account. For example, if you have your money in a savings account at the bank for 0.01% while inflation is at +3.5% for the year, it means you are losing 3.49% of your hard-earned money annually.

Try not to stand flatfooted out here while high-interest savings accounts are going for plus 5% and bonds north of 7%. There are asset classes that perform well in inflationary environments. For example, tangible assets like real estate and commodities. Others typically suck like tech, which may lead to a BUY moment.

It’s all about how you want to approach long-term investing. If you can’t invest, pay down more debt, or save more money. Most people make the mistake when thinking everything will stay the same. It won’t. And about Date Nights. I feel sorry for your single folks, ie, casual drinks and an entree will break you at $100 plus tip. It’s madness. Stay home and invest.

Check out our TNFG portfolio on Google Sheets if you want to see a full breakout of our portfolio.

Building Toward Our May Goals

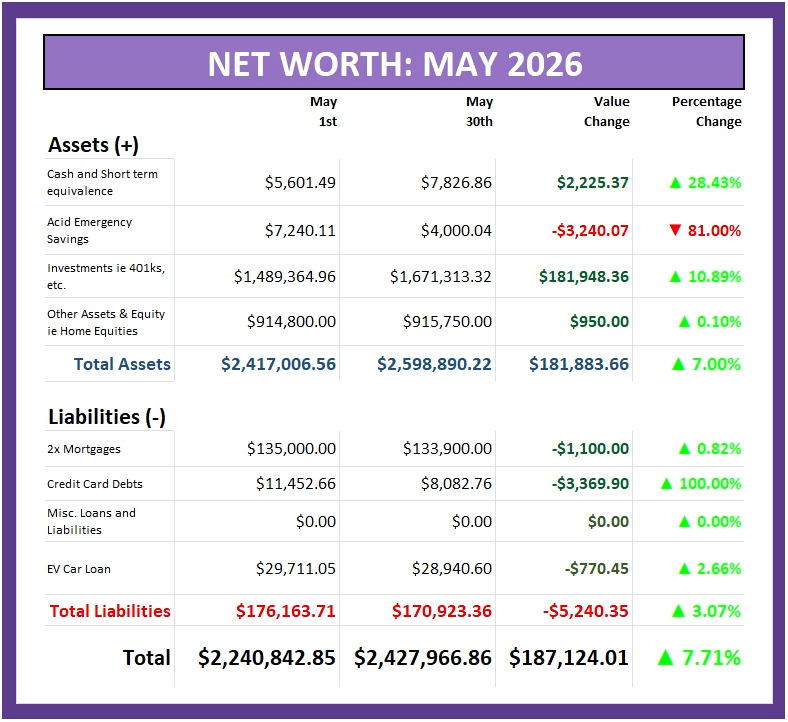

Back to business. If you are new here, this blog post is all about TNFG’s monthly Net Worth Breakdown for May 2026. Additionally, there are always usable financial nuggets and aha moments that might help you along the way.

Strategic Changes from May and Beyond. My wife’s birthday trip was a solid success. There is something to be said about a mid-term break to reset and recharge. We have two months to set up our new tenants for the rental property. Beyond tightening the war chest for Peru (Fall 2026) and Brazil (February 2027), it’s GYM TIME.

Our goal is to end the year with over $1,750,000 in our investment portfolio. We are on the razor’s edge of spending as the Mrs contemplates taking a pay cut and a new gig. There is no chance to close the year with no credit card debt, but hopefully the investments make more cents. Once we kick off 2027, we will try to knock down the RE mortgage ($900) and the car note ($900). By 2028, we will have a total of $1,000 to throw at the primary home and $1,000 more to investments. Either way it plays out, the future is looking promising.

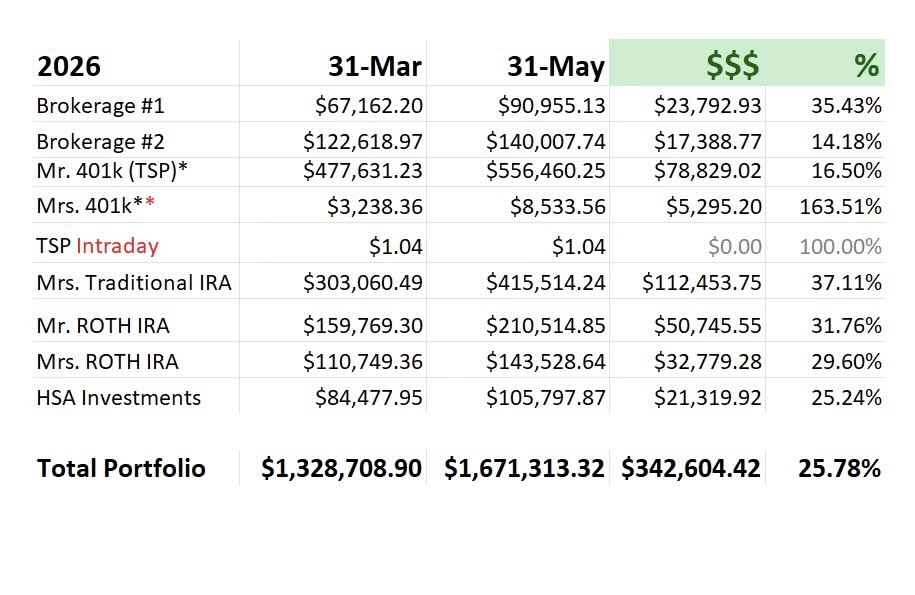

Here’s a quick summary of our net worth so far:

All in all, +7.71 percent, which is better than zero. The cash value grew by $187,124. This is beyond my expectations. The market was on a downward slump (created by Trump) in Q1. We are clawing our way back like Leo DiCaprio in The Departed. Turns out, the Bulls are beating the Bears. The wealth ratio is incredible. Making more money with our investments ($76,793/month) than our gross salaries ($21,667/month).

Investing is mandatory if you want to buy back your time. For every $8 we earn, we spend $2.50. We pocket at least five dollars in this equation. Those five dollars are then invested in the stock market. Wealth is simple arithmetic at this point.

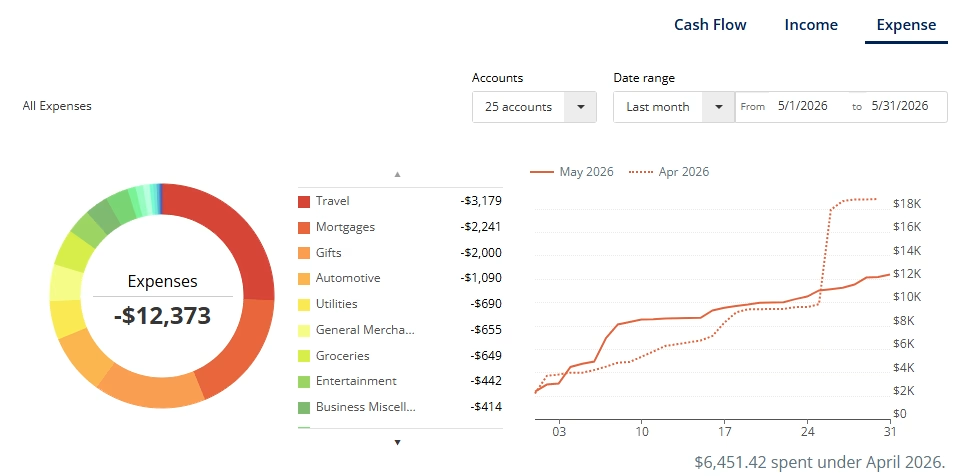

Our Expenses for May 2026

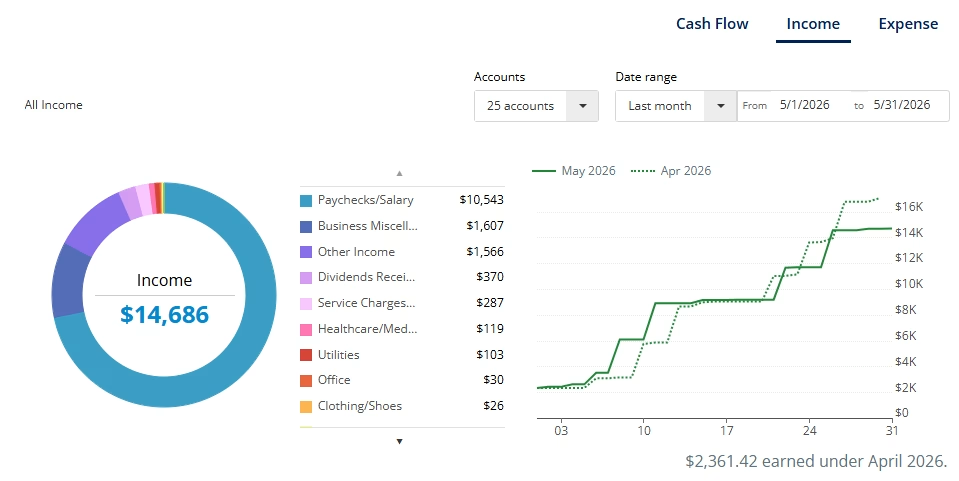

While I miss the way Mint.com laid out expenses, the cash flow screenshots from Empower do the trick. Due to travel, we spent the least on food (in months). Our Food & Dining budget typically ranges up to $900, but we settled at $661.

Our total travel hit $3,169. Mexico City felt like Latin America with North American prices.

While the 1-week vacation wasn’t expensive, it wasn’t as cheap as I had anticipated. Lessons learned, and fun was had. Work stress has consequences, so building in vacation time does help. You don’t even have to travel.

Sometimes going around our city can hit the spot, just be sure to use your PTOs liberally.

Our last tenants were great, but they are leaving (normal college town turnover). We locked in new tenants for the same price. We aren’t slumlords or real estate barrons. The rental is here to park cash and provide a spot if the kids in our family decide to go to FSU. Now we have to do a road trip to clean up the space, which will cost around $1,500.

We pocketed $1,909 in dividend income year to date. Other bills were OK as well. See the images of our cash flow income vs expenses.

1. So, where were the May wins?

In order, Debt Repayment, and that’s pretty much it.

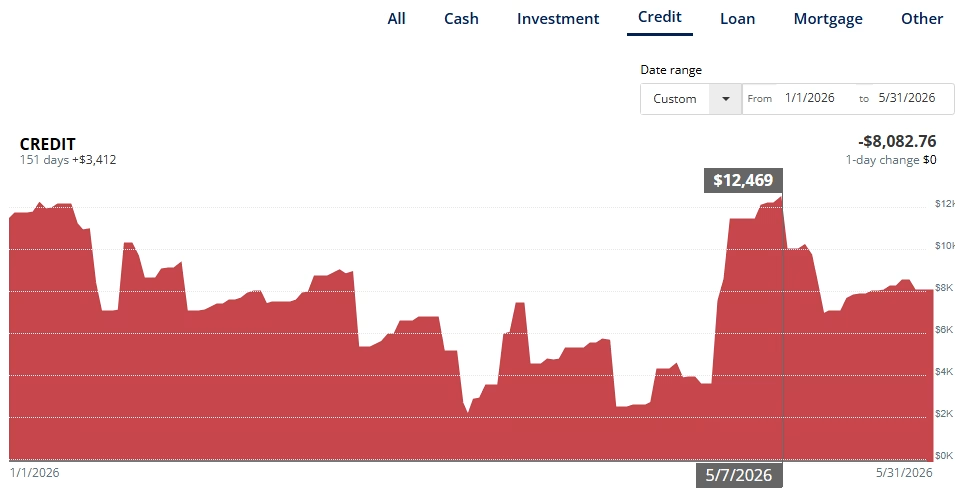

Debt Repayment in 2026 isn’t going as planned, but it’s progressing. The goal for total debt repayment is $81k in 12 months. This month’s total liabilities decreased by $5,240 (3.07% improvement). The credit card balances total over $8,000, but our FICO scores are amazing. If we have extra dollars, we sneak in a few extra payments to the principal. The next phase, post-2026, is to throw in a dedicated +$250 per month?

We are using this time to prep for more debt. I know a lot of people are afraid of debt. For the wealthy, it’s all about cash flow. If we can make more money on our investment versus our debt’s interest, it’s a smarter play for wealth.

Bumpy road for investments, but positive nonetheless.

We pulled in over $340,000 in investment growth from March 31 to May 31.

Minus the contributions for the month (i.e., $32k), it’s a $308,854 increase. It pays to be invested in forward progress. If you need tips on how to set up a solid portfolio, read How to Build a Long-Term Investment Portfolio Earning 250%.

Cash holdings increased a little

The end-of-the-year savings goal is set at $10,000. We are currently at $4,000, but we will boost that number in December. How? Our Acid Emergency Plan. I’m telling you, the net/max financial plan hasn’t failed us yet.

2. Where did it go wrong? And does it even matter?

Food, Fixed Costs, and Unintended Expenses

As stated earlier, we can’t control food costs due to inflation, shipping costs, and global labor shortages. My wife and I had a chat about our financial blind spots. Being prepared beats being caught off guard. The Boomer parents are running short of catch. My mom asked for $2k, which stung a bit, and my dad-in-law is entering financial constraints. The Black tax is real.

The cost of life, things are just blowing up left and right. And we still need to do some repairs. We are getting rid of the old car, which should help our insurance prices. And our mortgages are $2,000. Our fixed costs are $3,000 per month before anything. I’m saying all this because most people don’t know how much they are spending. That’s where it can catch up to them.

Make sure you are aware of your cash inflows and outflows. You want to be at least $500 per month to be financially stable. Quadruple that and you will be a millionaire in no time.

3. What is the Next Step for Us?

The fall trip will be in Peru with a detour to Colombia. Neither shouldn’t be that expensive. Time to get back in shape for Brazil’s Carnival festivities (early 2027).

Beyond that, here are our overarching goals for 2026:

- Keeping our expenses where they should be. “So stop equating happiness and social acceptance based on the money you spend.“

- Get to $100,000 in M1 Finance, focusing on Growth and Dividend Income that generates at least $4,000 in passive income in 2027.

- Check out the portfolio in real-time. If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate with the push for a $2 million portfolio by February 2027.

- To help monitor your savings, cash flow, net worth, investments, retirement, etc. All FREE with Empower, formerly Personal Capital! Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

About Author

{kind=link}

2 Comments

Dolla Lady

Thanks so much for your writing over the years Lawrence! Following inspiration from you and other educational voices, I hit Coast FI this week 🙂 $510K invested and 25 years to go until retirement! Congrats on your success, and keep up the great content!

Lawrence Gonzalez

Thanks. Most of the time, it feels like I’m writing for no audience at all. So it’s great to hear that at least someone has benefited from this. Cheers to your continued success. It’s going to get easier going forward.