Not Debt Free But On Track to $2 Million Investment Portfolio

June 2026 is now over, and thank God for the Q2 rebound.

For a second there, gas prices were spiraling up, and Iran held up the Strait of Hormuz (that’s still happening, by the way). Due to continued standoffs, there have been ongoing threats to shipping, including Iranian plans to charge service fees for passage. This accounts for the surcharges that you’ve been paying in energy and at the pump. The heat dome over Europe isn’t helping either. When the French are fighting like it’s a 1998 Black Friday sale for ACs and fans, you know it’s bad.

We were on the brink of another social media-proclaimed recession (for about 2 weeks). On top of that, inflation remains sticky post-tariff reversal. America is broke and needs to get on the Ramsey solutions for the debt-free scream. Alas, the people aren’t interested in cutting back; instead, we are out having “Big Fun.”

Fortunately, investments pivoted since liberation day (tariff day, April 2025). The S&P 500 gained 33.13 percent from the start of April 2025 through June 30, 2026. Driven heavily by a continued capital spending boom in artificial intelligence and technology, the index rallied strongly through 2026. So much so, the S&P 500 gained almost 15 percent in Q2 2026 alone. With the wind at our back, we aren’t out of the storm yet. Retail investors are fearing up to three federal rate hikes. And nearly one in three Americans isn’t saving at all. The future is getting expensive (plus taxes and fees).

I say, “let the FIFA World Cup 2026 good times roll.” Time to link up with friends and head to your nearest body of water to cool off.

Table of Contents

The Big Winners for the First Half of 2026?

Big winners for 2026 are those who bought the dip on March 31.

Tourism is up again but with a twist. The “K-shaped” split is defining summer 2026 travel. High-income earners are splurging on experiential, premium travel. Budget vacationers are opting for local venues, i.e., bars, pools, and anything 250th-related. Gone is the discretionary income for most families. Major sporting events like the World Cup and the NBA Finals offer premium seats as high as $7,500. The bulk of the fans are partaking in activities outside the arenas. People were even braving heat exhaustion to stand outside Madison Square Garden for the coronation of Taylor Smith and her consort.

Yet it’s still early, so we will likely see more domestic road trips in July. Key trends include “coolcations” (escaping to cooler climates), “set-jetting” (travel inspired by movies/TV), and a major surge in nature-based outdoor escapes. Nothing can beat free.

Sandisk $SNDK and data storage stocks carried the market for a good month. Bitcoin spiraled below $60,000. Some stocks are soaring +100% this year. So far, fear and greed are eroding market fundamentals. I expect violent rotations from tech to non-tech stocks. Consumers are faring worst. US households owe $18.8 trillion in debt (refer to Household Debt and Credit Report – Q2 2026). A troubling number, as the Big Beautiful Bill (#BigBackBill) comes into the ledger.

We are in a DEBT spiral. Consumerism remains unabated. This is not a drill. The Federal Reserve continues to eye long-term prospects for rate hikes. This means additional job cuts. Depending on the industry, you will be looking at at least 5-6 months before landing a new gig.

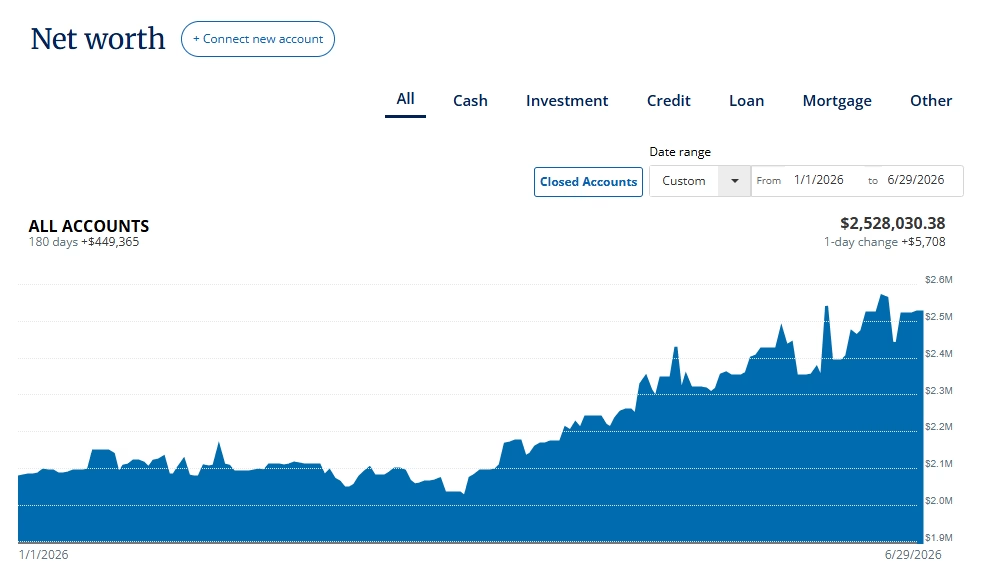

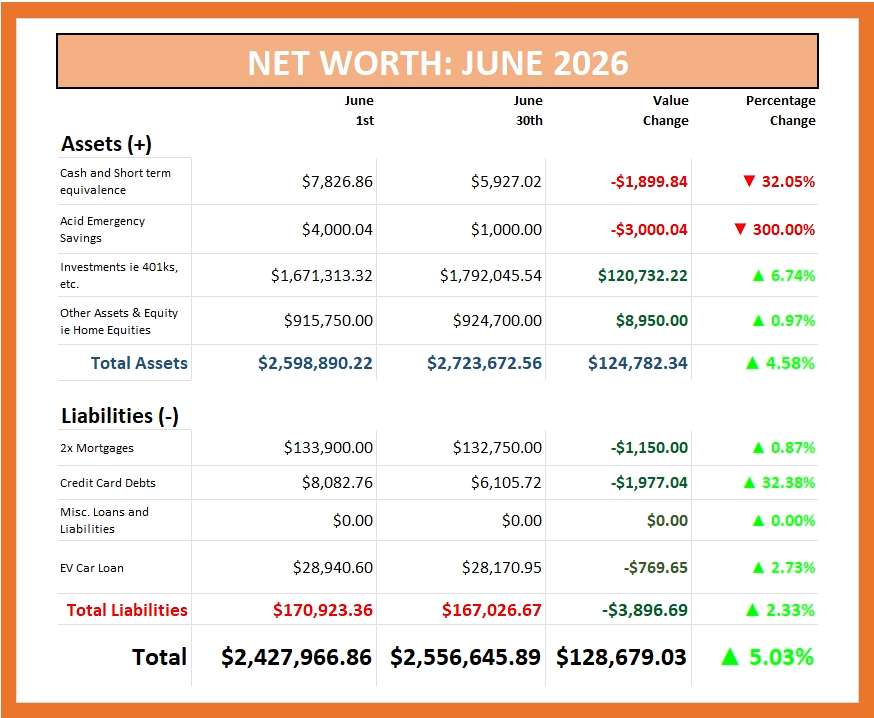

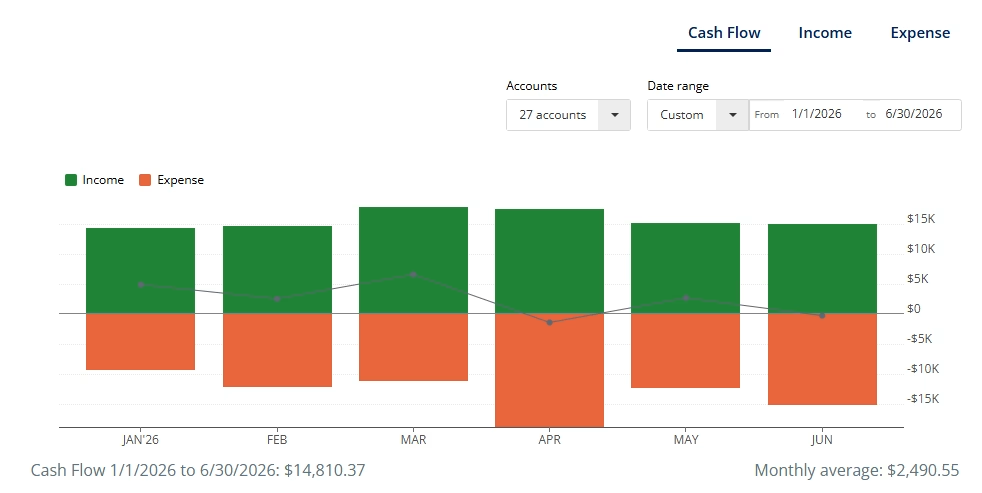

We are on the way to the end of another year with the market north of 10%. If you didn’t get the memo, “You have six months to get active.” To do so, you have to start reviewing your finances. Most wealth building happens in the mind first. The TNFG household made +$60,000 in debt payments while being short of +$33,500 in investment contributions during the 1st half of 2026. Even those moves added $90,000 directly to our net worth. In total, we netted +$500,000 YTD. We will break the data down further.

Half-Time Rally – Time to Build Wealth and Pay Bills

It’s unsettling how most months fly by in a maelstrom of confusion, politics, finances, and now the World Cup. I highly recommend that you take a mental health break whenever possible to recalibrate and allow yourself to heal.

For the last six years, I warned people of high prices. It wasn’t until we took the trip to Switzerland and Portugal (2025) that I noticed these tariff prices are global. Meaning what costs us more in the US causes prices to trickle upward elsewhere. We are definitely in the same global economy.

Those high prices were primarily spurred by global demand, which increased the need for higher interest rates. This culminated in high loan payments. Mexico City felt like it was in South America but with US prices. Brazil’s prices also started to adjust up. The more influencers pop up, the higher the prices.

The median car loan is pushing $1,000 per month. We purchased a new $50k car in 2023, with the monthly payments of $893.59. To make matters worse, the insurance adds another $266 per month. That’s a nice balance of $1,159.59 owed monthly.

While you don’t have to buy a $50,000 car, you will buy one later. In the US, the average age of vehicles reached a record high of 12.8 years. These increases are unavoidable.

My problems aside, I can tell you that prices aren’t going down. Price inflation (the rate of increase) is slowing down; however, this isn’t Disinflation. Meaning prices aren’t going to roll back. More people are vying for the same products with less supply, which equals higher prices. Your best bet is to go leaner. Minimalism works. Balance your budget and your diet, and opt for more enriching experiences.

We can’t be too cute in this economy. Making financial mistakes (over 30) is taxing.

So, will we be consumer debt-free? Nope!

We try every year, but between travel and unexpected expenses, we fall short. Things keep breaking, and repairs are needed. From car purchases, trips to the vet, to AC repairs, life tacks it on.

Our 2025 trip through Switzerland and Portugal cost around $15,000. The next trip to Brazil for Carnival 2027 looks to be $20,000. At some point, we found ourselves throwing money out of the window to see if it sticks. Hotel prices have been red-hot this year. Overtourism might be a thing, especially with influencers telling everyone about our favorite locations. Even as our annual travel costs near $30,000, our investments are also growing. Our investment (net of contributions) grew by $400,000 for the first half of the year. That’s 1.5x our annual gross salaries.

The adage is true: buy the assets on the front end, so you don’t have to worry about wealth on the back end. My wife and I were making money while taking a hot air balloon ride over Mexico. I can’t stress the importance of pivoting and creating breathing space.

Your budget and goals must stay flexible. Never know when an unexpected cost may pop up. Try not to overspend in the interim, especially when times are good. Prep now, pay off what you can, and invest the difference. You don’t have to spend all the money that you earn.

With all that said, our household net worth managed to reach $2.5 million. Of which, our investment portion totaled +$1.75 million. We have a shot at $2 million in our combined portfolio by year-end.

Quick financial tips

The only intuitive way to stop bleeding financially is to buy or spend less through the end of 2026. If you have loose change, invest more while the market is down, because millionaires are born during recessions and downturns. Additionally, if you have student loans, check out the latest Federal Student Loan reform changes. Read the Department of Education’s Press Releases and ask questions.

One big lesson to consider is that if you have your money in a savings account at the bank for 0.01% while inflation is at 3% for the year, it means you are losing Negative 2.99% of your hard-earned money annually. While banks are even dishing out more dividends to their investors.

As of July 3, 2026, JP Morgan & Chase’s $JPM is up 16% over one year, vs the Chase Savings℠ account interest rate is 0.01% APY (effective 7/03/2026). I wish I were making this up. And it doesn’t include the dividend yield of 1.77% quarterly. You would have made more money by investing your money in the company instead of in the product.

Can’t say I didn’t warn you; you can’t save your way into wealth.

Here are our 2026 Total Debt Repayments YTD

Table 1. TNFG Mid-Year Debt Repayment Recap 2026

| Credit Card Payments | Interest Incurred minus CC Rewards | Mortgage Principal Repayments | Auto Loan Repayments | Total Payments | |

| January | $9,651.64 | +$742.05 | $1,000 | $762.31 | $12,156 |

| February | $9,250.85 | -$265.41 | $1,000 | $756.52 | $10,741.96 |

| March | $8,045.49 | -$215.37 | $1,000 | $764.08 | $9,594.20 |

| April | $7689.11 | -$546.88 | $1,000 | $775.66 | $8,917.89 |

| May | $7,243.49 | -$287.74 | $1,100 | $770.45 | $8,826.20 |

| June | $9,222.19 | -$84.59 | $1,150 | $769.65 | $11,057.25 |

| Total | $51,102.77 | –$657.94 | $6,250 | $4,598.67 | $61,293.50 |

How much have we invested to boost our net worth as of June 2026

Grand Total (a clean) $33,500 (Refer to Table #2). While the global pandemic has become old news, the world is still looking over our shoulder at Russia vs Ukraine, and the unstable Middle East. The Federal Reserve is aiming for further rate hikes, but we have to get through the political noise.

Only the future will tell; however, I suspect that a rate hike won’t come until September 2026. Either way, “Can’t debt freedom your way into wealth.” You have to have a great strategy that incorporates both debt repayment and investing. This is why I share the Net Max Financial Plans for FREE.

Table 2. TNFG Mid-Year Monthly Investment Recap 2026

| Employer Investments | Additional Invts. Contributions | Total Investments | Holdings Performance | |

| January | $5,000 | $575 | $5,750 | +7.44% |

| February | $5,000 | $0 | $5,000 | -0.23% |

| March | $5,000 | $925 | $5,925 | -3.58% |

| April | $5,000 | $500 | $5,500 | +15.29% |

| May | $5,000 | $500 | $5,500 | +15.28% |

| June | $5,000 | $1,000 | $6,000 | +5.6% |

| Total | $30,000 | $3,500 | $33,500 | +45.05% |

Celebrating the Next Half after Surviving the First Half

TNFG’s monthly Net Worth Breakdown for June 2026 was wild.

Pending rental conversion and travel expenses are pushing us hard, but the market is pushing back. Our investment performance for the year so far is solid. We will happily take the 20% instead of a recession. Refer to the annual performance graph above.

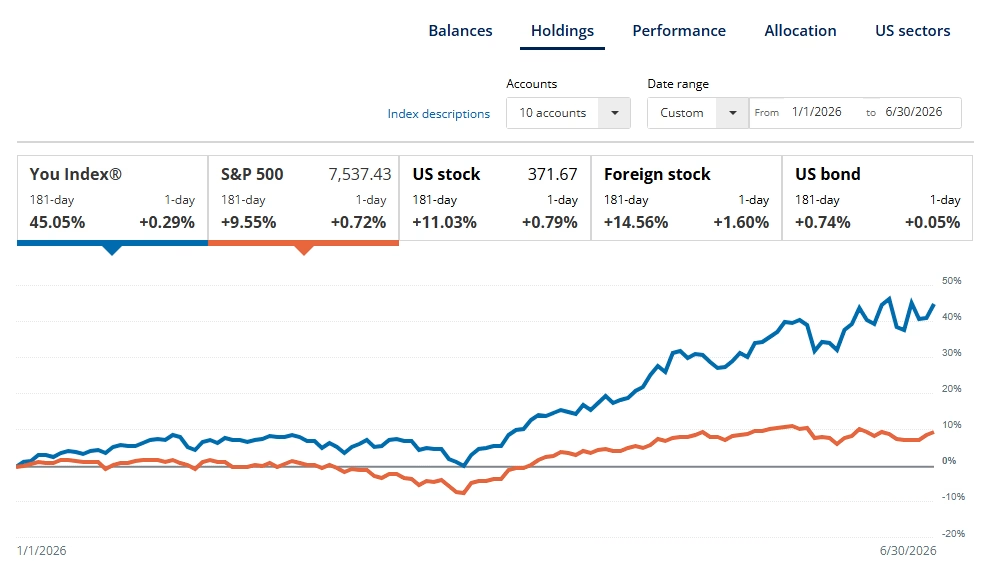

Over six years, our holdings are hitting +208.47 percent over the SP’s 146.34 percent for the same period (6/1/2020 to 6/30/2026). That’s an average annualized return of 34.75%. Not too bad for long-term investors.

Bonus for all the readers: if you want to get a near-accurate view of the TNFG Investment Portfolio with all the holdings, click because it’s blue. It will send you to the Google Sheets view. People ask, and I always deliver on transparency.

Pushing FWD into our next trip to close out the Year

First, I would like to express my gratitude. This year, we were hit with micro expenses. Those tend to add up here and there. The extended winter was a bit strenuous, and the heating/cooling costs were higher than anticipated. It comes down to recalibrating portion control, gym scheduling, and more importantly, sleep. We came back from the Mexico City mid-year trip with a better understanding of the people and the culture. We have one more international trip to Peru/Colombia in the fall with two domestic trips (July/August).

My wife and I are finding synergy (along with Brownie, our dog). With new renters for the upcoming academic year, I have to head south for the cleaning and turnover. The back half of the year will still be challenging, but we are here for it with gratitude.

Here’s the Quick June 2026 Summary:

What Happens Next!

“We are in the endgame,” referencing the Avengers’ blockbuster movie. In more ways than one, 2025 was a readjustment, but we are making strides to get to the $2 million net worth mark.

June 2026 ended with +5 percent. The cash value grew to over $120,000. Investments dribbled better than Dennis Rodman’s daughter. Now we are hoping for a solid 2nd half (+10 percent) investment performance.

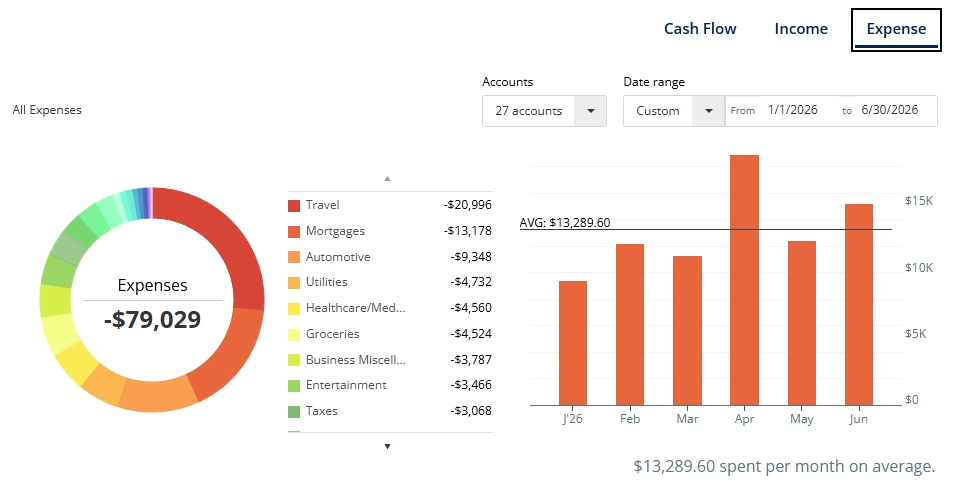

Our Expenses so far Mid-Year 2026

It was Mrs’ birthday month!

Credit to the wifey for keeping expenses and excursions low. After that, it was brisk walks and museums in Mexico. Beyond that, we finally got a slight hold on our food costs. I’m changing my diet radically and getting on the Fitbod app in Q3. You need to eat less to lose weight and build energy. Then, you need the energy and rest to lift weights. It’s a vicious cycle.

The hope is that we establish a baseline for the next six months.

Our goal is to prepare to purchase a new home in 2028. Every adjustment helps, especially since we are looking at $30,000 worth of renovations (in our primary). This should boost the value, and it is looking like a $200,000 tax-free profit when we sell.

Give it (your budget) room. Eat out a little and ease back on the journey. Your budget should work ‘with’ you and for you.

Deeper Dive into the June Net Worth Numbers

Credit cards are being repaid, and our FICO scores are higher

Will Investments Continue to Rebound? (For Now)

We currently have an investment portfolio of $1,750,000+. FAT FIRE range if we keep this momentum through 2028.

In the second half, we are rebalancing into some index ETFs. I think the back half of 2026 might yield an extra +10 percent. Time will tell. If you need tips on “How to Build a Long-Term Investment Portfolio Earning 250%.”

So, what are our next steps for 2026?

What’s the deal for July? Nothing but Fireworks and Vibes

Preparing for a trip in August. The summer heat is not going to play, so way more sun rays to acclimate. Making changes to our investments in anticipation of the downturn in Q3 2026.

Beyond that, here are our overarching goals for 2026:

- Keeping our expenses where they should be by “Not equating happiness and social acceptance based on the money you spend.“

- Get to $100,000 in M1 Finance (by YE 2026), focusing on Growth and Dividend Income that generates at least +$3,000 in passive income by year-end. Check out the portfolio in real-time. If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate with the push for a $3 million net worth by Fall 2027. To help monitor your savings, cash flow, net worth, investments, retirement, and more FREE with Personal Capital! Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

About Author

You May Also Like

All About Making Millionaire Money Moves

Seven Money Principles to Grow Your Net Worth Faster

{kind=link}