Experiencing the Impact of the Financial Wall

No one prepares for the financial wall. It’s not just one of them but a set of micro thresholds that can have a positive or negative impact on your psyche. Like failures, there is always a cost for success. And today, we made +$75,000 on a day in the market. My hands were shaking…

To be clear, it wasn’t a violent shake. It’s a slight, unsteady awareness that you might have gone too far. Or more accurately, further than you ever imagined. I mentioned this to the ladies on our financial podcast, “The Financial Griot.” I think we are mutation. Some deviant strand of what you should be. It might even come from the trauma of growing up on the opposite side of the tracks. Genuinely, I was poor enough to understand that I couldn’t ask for more.

Society tells that to poor people. It’s good enough, and then you are thrown into church to absorb the idea that the struggle makes you somehow worthy. For me, it feels like any breakthrough will be insurmountable, and that I should be happy at the bottom.

Table of Contents

The 1st Wall of being Unremarkable

My family is very unremarkable. I don’t have many pictures with them. My father was absent, so I was never formally taught confidence and purpose. On the other hand, when my mother was around, she wavered between violent and timid. Her example told me repeatedly to keep my head down. I recall my godmother telling me to never smile in photos. I’m still not sure what that was about. One of my aunts told me to turn a blind eye toward aggression and violence. This almost got me beaten up. Collectively, they attempt to instill in me the virtues of a loser. Someone who goes along with anything and bows at the scraps, all while reciting that “God will provide.”

I don’t call them, and they don’t call me.

While I think I should be bothered by this, I’m not. My hands are steady. To me, they are boring, and to them, I’m complicated and chaotic. I’ve always been one of the black sheep. I want more, and they want less. They are afraid of the wall. If a challenge comes their way, they tend to back down and turn back. Hiding for them is a comfort. I accelerate.

This doesn’t make them bad people. It’s the opposite, I’m the deviant. They have a rubric, and they stick to it. Why mess with the recipe? I’m the one who didn’t want to stay where I was planted. As such, my hands shake at the precipice, an awareness instilled in me while I served in the United States Marine Corps. The first wall is yourself. It’s an abyss. There is no sound, no beginning or end to it. Most can’t deal with the silence.

To make peace with and venture into something new, it’s terrifying. And, it should be.

Toward the Next Financial Wall, Post-College and Broke

We are seeing a lot of articles discussing post-college unemployment. It’s nothing new, especially for Black men. In January 2026, Black unemployment was at 7.5%, 1.4% higher than one year ago. Periods of high inflation hit us quicker and more severely. On more than one occasion, I remember periods when 1 in 4 black men were gainfully employed. I went through this in 2008 (after undergrad) and 2012 (after failing out of Graduate school). Opportunities weren’t there, and yet I still needed to get over the wall. This is where you realize you have no money and likely a ton of loans.

For many, this is a make-or-break moment. You can fall behind for years. By the time I took stock of this, I was 29 years old. All my skills and abilities, the challenges and struggles had to amount to something. Yet no opportunities materialized. I played my cards all wrong with no roadmap. If you venture into yourself and find nothing but excuses and scapegoat your issues to others, the finish line has already arrived.

Back then, my hands were shaking because when I reached, I found nothing.

I was confused, but that was the point. There was nothing there to hold onto, nothing to unmake, nothing to refine. It was easier to accept that at that moment, I needed to make something of myself without society’s input. I took a low-paying job and began transforming myself.

It was the absolute zero. I can work with that.

The Next Phases of Financial Development

The break-even point came when my total assets cancelled out my liabilities. The process took six years. On paper, I had nothing, and most importantly, I owed nothing. I was a blank slate to the universe. It was freeing and filled with potential. I shifted toward traveling the world, which led to a homeownership opportunity. Met my future wife in the process, and the rest was history.

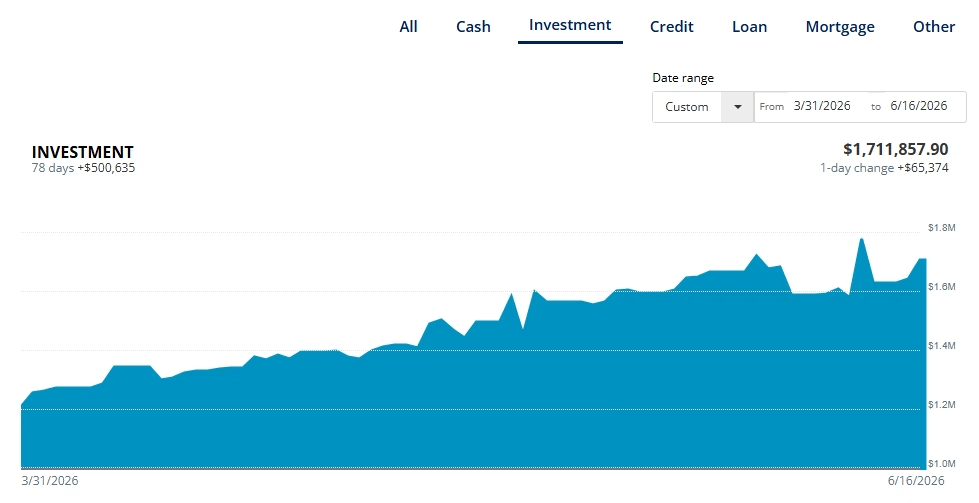

Subsequently, we were able to get to the first $100k in our total investment portfolio. This cemented that we were on the right track. Even though we weren’t sure where it was going. My hands steadied. And then we hit the improbable $1M net worth and eventually $1M in investments (November 2024). That’s a good 10 years from $0.00.

Now we are getting closer to the final wall.

The $2M Climb to the Other Side

I theorize that if you have this much invested, you are guaranteed financial stability short of something catastrophic. With every step before you, you should have learned discipline, purpose, and ultimately self-mastery. But this step is gigantic.

Hitting two million in investment translates to what most millennials will need to live off in retirement. Whereas most people will have less than $250,000 to work with if they are lucky, even if we stopped today, we would be just fine.

Here’s a chart of what $2,000,000 looks like invested at 8% at different time periods:

| Total Interest Earned | Total Ending Balance | |

| 5 years | $938,656.15 | $2,938,656.15 |

| 10 years | $2,317,849.99 | $4,317,849.99 |

| 15 years | $4,344,338.23 | $6,344,338.23 |

| 20 years | $7,321,914.29 | $9,321,914.29 |

| 25 years (std. retirement) | $11,696,950.39 | $13,696,950.39 |

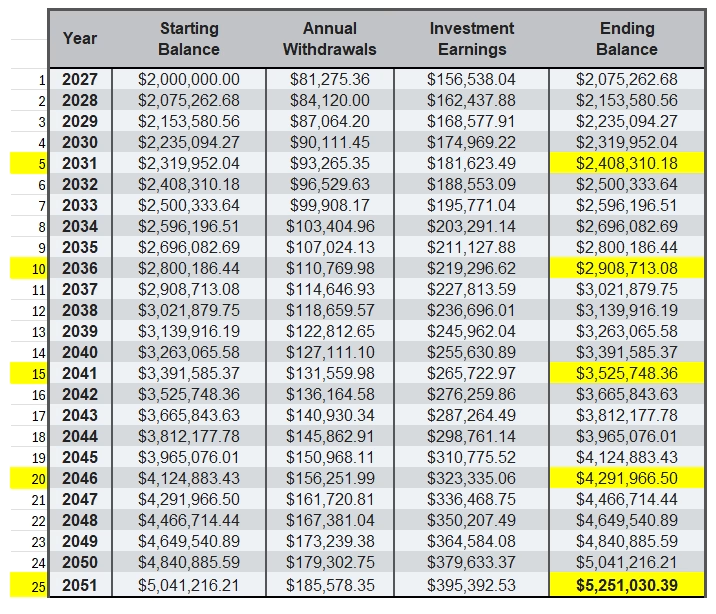

Here’s a chart of what $2,000,000 looks like if we retired and used 4% ($80,000 + 3.5% annually increase) while staying invested at 8% (at different time periods, cumulatively):

| 4% Withdrawal w/3.5% annual increase for Household Expenses | *Average Annual Withdrawal for Context | Total Interest Earned | Total Remaining Balance | |

| 5 years | $435,836.36 | $87,167.27 | $844,146.54 | $2,408,310.18 |

| 10 years | $953,473.23 | $103,527.37 | $1,862,186.31 | $2,908,713.08 |

| 15 years | $1,568,263.46 | $122,958.05 | $3,094,011.81 | $3,525,748.36 |

| 20 years | $2,298,441.39 | $146,035.59 | $4,590,407.88 | $4,291,966.50 |

| 25 years | $3,165,663.72 | $173,444.47 | $6,416,694.10 | $5,251,030.39 |

Basically, this is why my hands shake…

The magnitude of this is unreal. If we do nothing, we win, and even if we get out of the game, we have the potential to win. This is the final hurdle from which there is no return, especially if you took hard lessons along the way. For my wife and me, the curriculum was set on extreme difficulty. At this point, we are in uncharted territory.

It makes it harder since we don’t really have anyone to discuss this with.

The median US Black household’s wealth is under $50,000, with a median stock market holding of $16,500. Without being celebrities, athletes, or high earners, we were still able to amass a sizeable portfolio in a relatively short amount of time. All while people in our peer group navigate high credit card debts, student loans, employment uncertainty, and even unemployment.

Yet, I take deep breaths. I steady my nerves and commit to consistently adjusting my expectations of the market. This is for the long haul. All our effort and focus have to amount to something significant and meaningful. So, for now, we set our goals to raise our cash on hand to $200,000 by Year End (YE) 2026 and then to $250,000 next year. Beyond that, we will keep adding to the puzzle through YE 2032.

We are riding the wind and chasing the unknown. It’s terrifying, and it should be. That’s how you know it’s worth something. We are scaling this wall. In the end, this is just my notes on how it feels to move beyond abject poverty, toward somewhere new. I guess I’ll have to see what household becomes because this is beyond my imagination.

I never looked up this much. Steady!

About Author

{kind=link}