How to Set Up $2.5M Financial Goal in 2026

My wife and I are back for another year of building toward our ultimate financial goal, retirement by year-end 2032. It’s a long shot, but it’s worth the effort. First, $2.5 million net worth in 2026, followed by $5 million by the end of 2030. Each goal works to brace the next. [Perceived] Chaos is truly a latter.

While I might have referred to the journey as a “season” before, a “quarter” (QTR) seems more appropriate for the long game. QTR 1 (2019-2024) was about the setup and foundation. The second QTR (2025-2030) will push us through the early retirement range. QTR 3 will be the trigger point (2031-2032), while QTR 4 is the full retirement journey (2033).

Based on our net worth and trajectory, we may fully retire by the end of 2032 (with $7 million). I can only see us extending this if we opt to adopt or foster kids starting in 2033. If that’s the case, my wife would retire fully, and I’ll work through 2037 (with $10 million). This might seem bold, given we started with a negative net worth of $108,077 (deficit) in 2014. We reached millennial multi-millionaire status in 2025.

While the last ten years have been explosive and marred by personal setbacks, we persevered. Our success is something we share with others. Knowledge of what’s possible is important. Even hoping and planning for an improbable future is extremely important. My wife and I have never known anyone who retired fully and didn’t struggle with resources. To us, this is uncharted territory. The American Dream is just an idea; the reality has always been one of work and adaptation.

Table of Contents

Anything is Possible If You Keep Your Financial Goals Flexible

For anyone new here, The Neighborhood Finance Guy writes about financial literacy topics such as How to Grow Your Wealth, Budgeting, Investment Strategies, Retirement tips, and more. The goal is to help you make effective decisions and set S.M.A.R.T+E.R. goals with your money.

Most people mess up their financial plan due to inflexibility.

You can plan for everything and still come up short. Those who understand that learn to take the hit as a learning opportunity and adjust. Stay dynamic; the cards will not always fall in your favor. Your efforts (unfortunately) will not be synonymous with your outcome. The game is about learned acceptance of the things that didn’t happen and gratitude for the things that did. I’ve lived a hard life, and with additional US Marine Corps training, I learned to be steady when others are frantic. My wife, not so much. She is way more anxious. however she is learning by experiencing life with me. A lot of people have forgotten adaptability, which makes their entire lives harder than it needs to be.

As always, the information is FREE, but the struggle is not sold separately.

Welcome back, TNFG fans, and any Newcomers

Cheers to the start of the new year.

Everyone will not get the chance to live through 2026. As such, communicate more and forgive the negative cycles. Bury the hatchets, or better yet, let your enemies go on their own path. No one said you have to coexist with them; the world is big enough for space.

There are a lot of people coping with escalating immigration attacks. Others are stuck seeking employment, with the time between averaging 11 months. Some are still rebuilding their homes in California. The year is already tough for many families and friends. Be mindful, and communicate.

Beyond that, working on a better financial future can improve relationships and lead to fewer issues. Since we were snowed in the Northeast, it was time to draft our 2026 game plan. Sadly, Budgeting and Net Worth Tracking aren’t the norm, but being normal leads to being broke.

With so many retiring broke and wishing that they understood personal finances, now is a great time to start. Time is the only true, fleeting natural resource. You only get so much of it to live on purpose and leave an impact (if you choose).

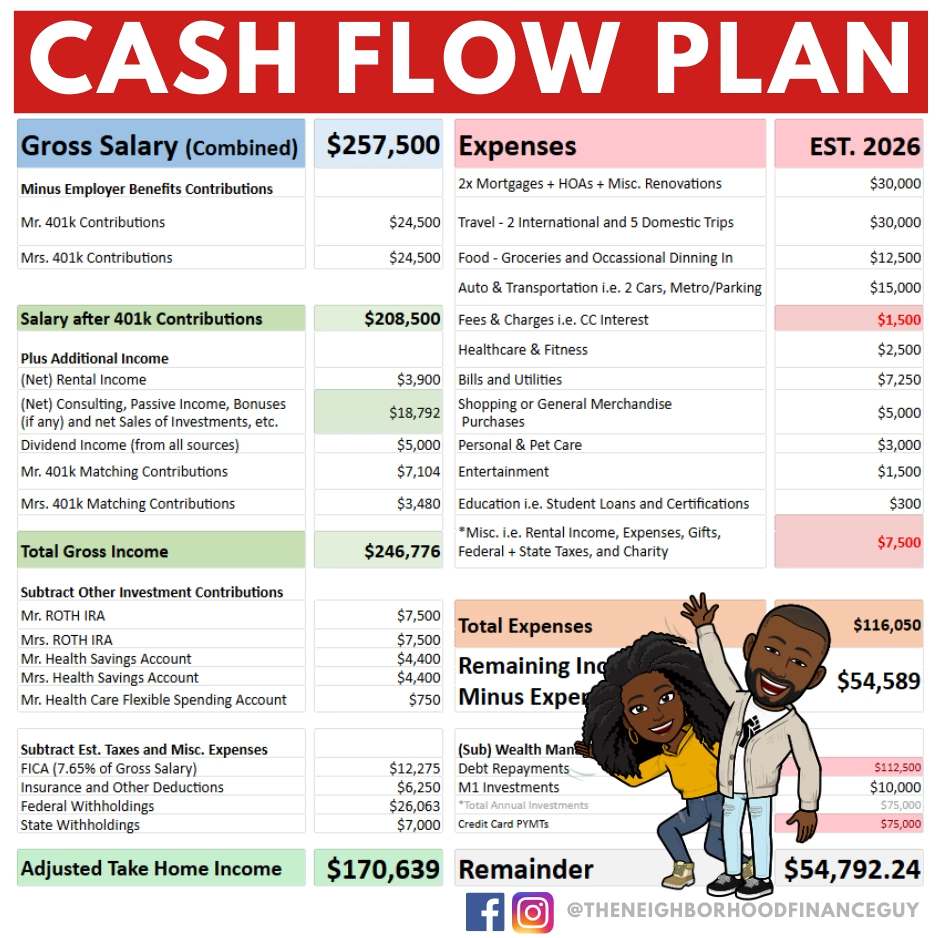

To reach your financial goal will require investing the difference

As for our household, my wife and I are starting the year with some much-needed introspection. We skipped the vision board in favor of three activities. One way to write out and share our big material wants in life. The second is talking about our top three (individual) objectives. And, finally, discussing the things that we want to do together.

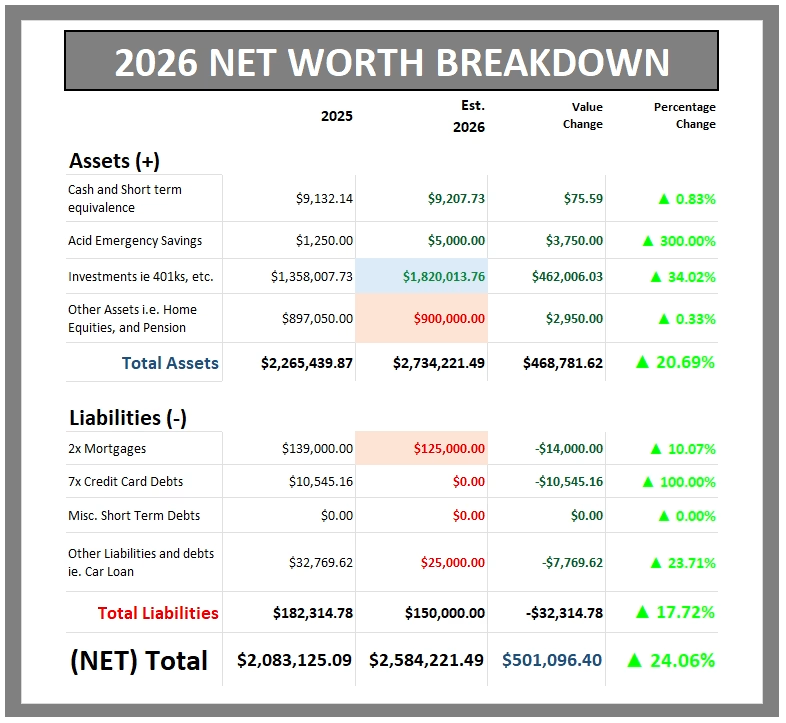

We added +$200,000 to our net worth in 2020 and 2021, respectively. 2022 slowed down to less than +$100,000 while 2023 clawed back a massive +$360,000. If you were tracking with us, we hit average millennial millionaire status in August of 2023 due to the Public Student Loan Forgiveness of nearly $89,000. We bulldozed our way to +$517,692 in 2024. While 2025 was more muted due to tariff shenanigans, we still added $449,296. This brought us to over $2 million in net worth.

All in all, the big lesson is that when quality stocks are on sale, you should lean toward a BUY. As long as you have a long-term perspective (aligned to your risk profile), you should edge out +10 percent annualized gains.

Now, we are setting bigger and bolder goals for the future. For one, 2026 is a close-out year for credit card debt. Secondly, we aim to sell our current primary in 2027. We’ve outgrown the 2/2, even though we are unsure if we can find something affordable in Northern Virginia. But it’s worth a shot. I definitely want some grass and a grill. The idea here is to think of a probable future and visualize the work you need to do to get there.

Feel free to check out the recap for December 2025, “How We Gained +$20,000 Worth of Wealth in December.”

Our Estimated Net Worth at Year-End 2026

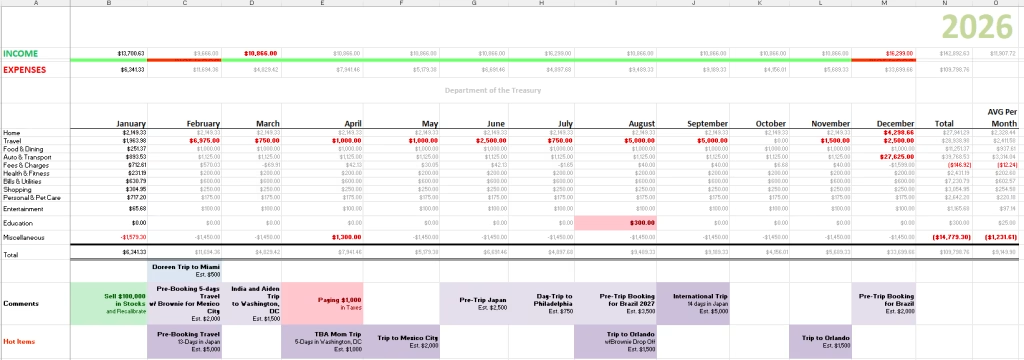

Our Estimated Household Expenses For 2026

Work Smarter, Not Harder to Write Your Financial Future

Since 2012, my wife and I have revolutionized our lives, so much so that we documented the entire process on The Neighborhood Finance Guy website.

I strongly believe that with the Net Max Financial plan, Americans can reduce the number of years required to work and become millionaires in less than 20 years. We did it in less than 6 years.

As bold as that sounds, understanding how money works can help you generate more wealth than your 9-5 ever could. It’s all about working smarter and not harder. Even if some doors close, focus on the doors you can open.

At this stage, I’m more concerned with netting +7% to keep up with inflation. Expenses are slated to increase by 30% in 2040; the struggling season is just beginning if people stay under-prepared. That’s what worked for us.

We are sticking with the long-term wealth approach. Social media is replete with get-rich schemes and zero-risk returns; the truth is that wealth takes time to build. You might not even see the fruits of it. This is why I strongly advocate wellness in association with building wealth.

Every new dollar is not as dreamy if you are sick, depressed, or both. Find financial stability, and you will find freedom. Cash flow management is the hidden solution that gets you on the path. With the net max financial plan, my wife and I gained nearly 40 cents for every $1 invested. As it compounds year over year, our future is limitless.

If this plan fails than it wasn’t good to begin with. But I doubt that it can fail, short of drug use. I’m literally that cocky about it.

If you need more information on wealth building, check out the Money Guy Show video below.

Building a Million-dollar Investment Strategy: Grow your wealth

We experienced our first super big investment drop of $50,000 in March 2020.

We stuck it out and found that long-term investments favor wealth. Once you establish your financial foundation and stability, the next part is just having fun. And once you master that, rebalance annually or semiannually.

If you do nothing else, INVEST in an ETF stock like $VTI, $VOO, or $QQQ. I found it more beneficial for people to be in the game rather than wait for the right time to jump in. These are all ways to grow your wealth. This might be the last great chance to buy great companies at a discount and to ride the wave to 2026.

Don’t get cute with trying to stockpick or cryptocurrency your way to financial stability. It doesn’t work. Try my patterned tips for increasing your household’s investment potential by 111%. I’m sure there will be more declines in the future, which will equal more opportunities for those who stay prepared.

Again, ETFs are a pretty simple entry point.

Invest in a SMARTER Strategy to Grow Fearless Wealth

Unfortunately, Dave Ramsey would disapprove.

When people are hyper-focused on paying down debt, they often overlook areas where they could have reduced their taxes, increased their assets, and secured their financial future.

Just as having the PSLF pay off (in 2023), for almost $90,000 for me, it was a better play to buy my time and invest the difference. In the end, I think I paid around $40k in student loan debt, in contrast to starting with $125,000. This is the definition of working smarter, not harder.

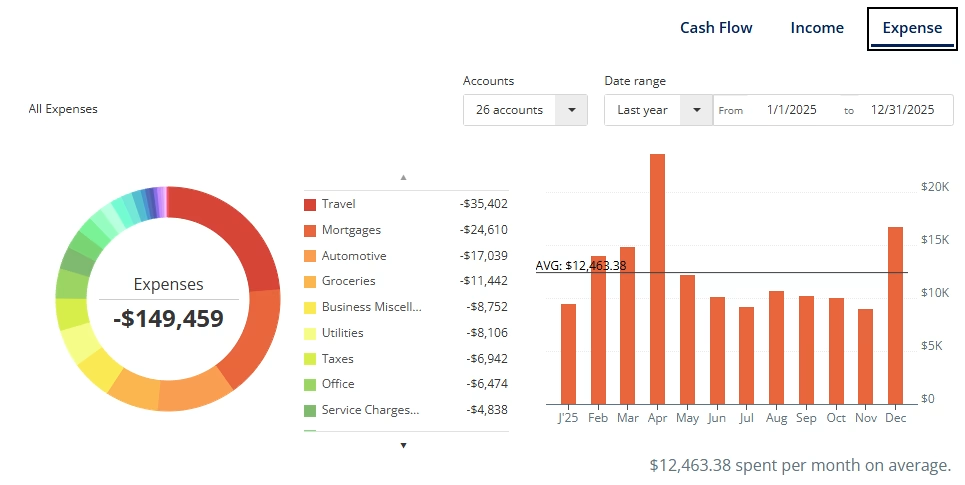

In 2025, we will likely spend over $35,000 on travel via credit cards. While packing credit card debt is generally a bad idea, it might be a reward card. It falls to how you manage money. Besides, travelling is our priority, so we decrease other expenses to make room.

In the end, the credit card companies paid us $1,750 in credit card benefits, cashback, and rewards. Not too shabby. We aren’t passing up on credit card reward points. With luck and no emergencies, we should be debt-free by year-end. We are very strategic with how we spend and invest to make up the difference.

Our goal is to reach wealth velocity while avalanching our way up. Inflation and high prices are hitting, but here we are. Wealth is (Contribution x Rate of Return) to the power of time.

This is why time is money. Your efforts today will compound tomorrow. Either positive or negative.

Estimated Net Worth Monthly Tracking

| Net Worth | Growth/Loss in Dollar Value | Growth/Loss as a Percentage | |

| January 2026 | $2,121,423 | +$38,298 | +1.81% |

| February 2026 | $2,112,326 | -$9,098 | -0.43% |

| March 2026 | $2,081,711 | -$13,371 | -0.64% |

| April 2026 | $2,109,730 | +$28,019 | +1.33% |

| May 2026 | $2,128,010 | +$18,280 | +0.86% |

| June 2026 | $2,129,523 | +$1,513 | +0.07% |

| July 2026 | $2,167,265 | +$37,742 | +1.77% |

| August 2026 | $2,234,196 | +$66,931 | +3.00% |

| September 2026 | $2,298,149 | +$63,953 | +2.78% |

| October 2026 | $2,317,858 | +$19,709 | +0.85% |

| November 2026 | $2,402,781 | +$84,924 | +3.53% |

| December 2026 | $2,500,000 | +$97,219 | +4.05% |

| Total Change | +$416,875 | +20.01% |

**Low Estimates for 2026 ($2.35M) and High Estimates ($2.55M)

***Post-Election Cycle, Expecting Turbulence in QTR 1-2 2026, Rebound QTR 3-4

Economic Predictions for 2026

Here are a few ways to Grow Your Wealth Like Us:

- Boost bank savings to $50,000 and keep 10% dividend cash reserves in investments to buy opportunities in 2028.

- To begin with, invest at least $500 per month in M1 Finance Brokerage focused on Growth and Dividend Income that generates at least $2,000 in passive income in 2026.

- Check out my portfolio in real time for pointers. If you like the platform and want to start investing, I have a $10 for $10 referral for added motivation – https://m1.finance/SYdqDJ2SyADC.

- We are shooting for a sustained investment rate with the push for a $2,500,000 net worth.

- To help monitor your savings, cash flow, net worth, investments, retirement, and more. FREE with Personal Capital! Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

- Work on personalizing the blog. Update the PowerPoint presentation. We are pushing to build out for the next 6 years [Net Worth Valuation $5M (2030)].

Disclosure:

This post is brought to you by the Neighborhood Finance Guy. We highlight financial literacy information, resources, and more on your way to money management goals and personal wealth. Our goal is to help you make S.M.A.R.T.+E.R. decisions with our money. We do not give investment advice or encourage you to adopt a certain investment strategy. Your ‘personal finance’ is up to you. If you take action based on one of our recommendations, we won’t earn a dime as of 5.2022. We operate independently.

Receive a selection of my favorite finds every week by subscribing to the newsletter. Make the Neighborhood Finance Guy website your trusted source for great content that will audit your life and rebalance your happiness and wealth.

Good Reads:

- Top Financial Literacy YouTubers for Beginners, and

- Top Financial Podcasts for Beginners,

- Top Three Apps to Make Budgeting Easier.

About Author

{kind=link}