Retiring Early vs. $3 Million: Is It Better to Keep Working At that Price?

Recently, I was asked, “Why would you forgo your highest earning years in favor of retiring early?” Obviously, I never thought about it like that. The infinite wisdom of a random social media commenter truly changed my life… Nah. For one, I don’t think they understood how meticulous I could be regarding financial planning.

I don’t know one person who retired and isn’t struggling financially, so I understand the caution.

Being second-generation Haitian narrows the number of successful retirees to an elite few. Do Haitian-Americans retire? Sure. Maybe? Have I seen it? Not really. Do they even have enough money to really say that they retired? Nope. Most of their bodies gave out. It’s as simple as that. They want to work and be valuable, but they physically can’t anymore. They were the first-generation that migrated to a foreign country with a resolutely diligent work ethic. Often, they were the definition of loyal employees. You didn’t have to give them promotions or raises. They were happy to have an opportunity. My mom worked at Walmart and would run to work at 4 AM with one impromptu phone call.

Coming from a country that lacked a banking structure, that generation made money and spent it. They only had one consideration: that they would be able to buy mythical land in Haiti, build a home or two, and then retire there to farm. Yeah, it’s a strange dream that’s far from the resort commercials with silver-haired models.

Currently, Haiti is a mess. That generation’s savings are less than $100,000 (on average) while their medical expenses are about to escalate. One of the few positives is that many purchased their home during the Clinton era.

Having grown up in Haiti, I always believed that going back to Haiti was a wild idea. When you migrate to a new place and settle for three decades, you will change, your tastes will change, and the place you want to return to will also change. Besides, leaving so many variables to chance hardly works out.

Watching and learning from their journey forced me to think of alternatives. I needed to figure out how not to work any longer than I needed to.

Table of Contents

Millions of Dollars on the Retirement Table

My wife and I are planning to retire in five and 1/2 years (I’m definitely counting).

By the time we kick off our retirement phase, we will have forgo nearly 10-15 years of our “prime-earning” years. These peak earning years would net the median American household north of $100,000 (annually), as much as $2 million. Since we live in the North East, our total compensation would reach at least $3.75 million. This total doesn’t factor in adjustments such as raises, bonuses, etc. After taxes, that could be a lean down to $3 million. No matter how you slice it, that’s a lot of money.

But it’s also a lot of time and calories.

Working sedentary jobs pack on calories and destroy your body. Just like the first-generation of Haitian Americans, you have to factor in that your body will change by the time most people retire. Turns out 65 is still 65.

Black (along with every other color) does crack eventually. The decision to retire ends up being a trade-off between your longevity, patience, and the almighty dollar.

Aside from that, I seriously don’t want to keep code-switching. It’s tiring and pointless to me. And due to my Latino origin, I require Cuban coffee in the morning. DC doesn’t have a Cuban cafe in sight. So, I guess we will have to part ways with that $3 million.

But don’t worry. We always have the Net/Max Financial Plan. Why does it work? Well, I designed it so that it does. But to keep it short, if you invest more than 25% of your gross pay, you will be able to grow your wealth in the market.

The results make you more efficient with your time, money, and taxes. Besides, I would rather do that than wait and find out. Nearly 50% of Americans have no retirement savings at all. That’s a recipe to keep working into your 70s. Nearly 3 in 5 Americans regret not saving or investing enough. Based on the economic cycle, it’s going to get harder to get ahead over the next twenty years.

So, How Will We Replace $250,000 Per Year?

Replacing a $250,000 gross household income is hard, but you technically don’t need to do all the heavy lifting. That’s the kicker. If your plans incorporate pesky elements, you should be able to dodge most financial surprises. One has to know how the retirement system works.

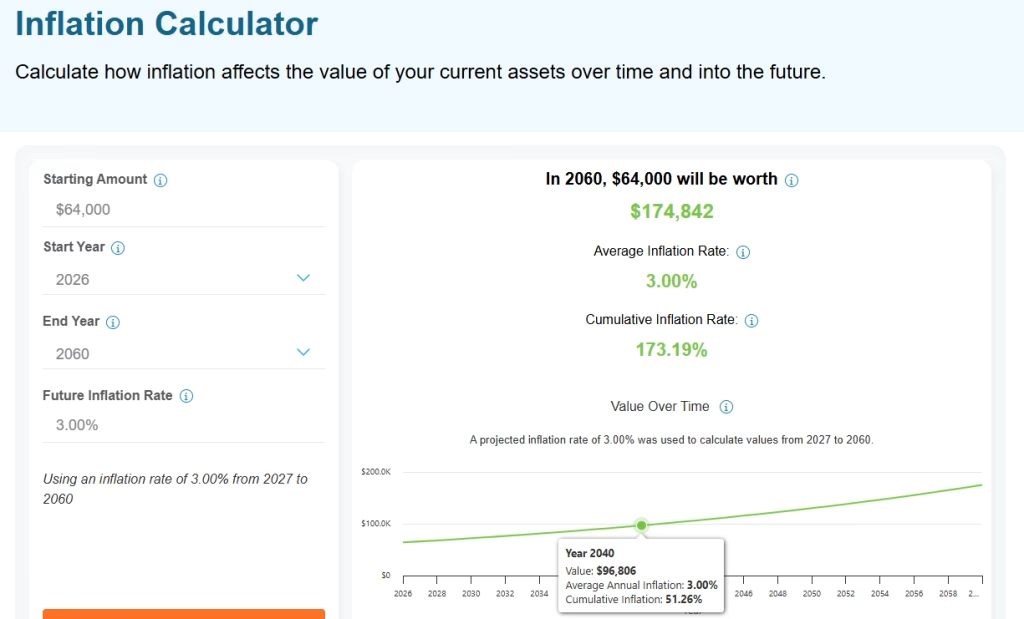

In essence, you need at least enough income in retirement to keep up with your current lifestyle while factoring in capital expenditures, medical expenses, long-term care, and inflation. That sounds like a lot. Give our take, you need 2.125x your current annual expenses.

If you are spending $80,000 now, that means you should plan for $170,000 by 2060 (see Exhibit A).

To make it easier, you need at least $2.7 million in savings as a millennial.

I’m an auditor and a Marine, so I naturally factor in everything. I’d recommend owning your home with the express understanding that you will make about $150,000 worth of repairs in retirement. It’s not too bad considering renters will pay nearly $2 million over 30 years. The property taxes are nothing compared to that.

This brings me to the famous three-legged stool of retirement. It’s the traditional model for financial security comprising Social Security, employer pensions, and personal savings/investments. It represents a balanced approach to funding life after work. Unfortunately, pensions have been phased out, and we will likely see tweaks to the Social Security retirement age.

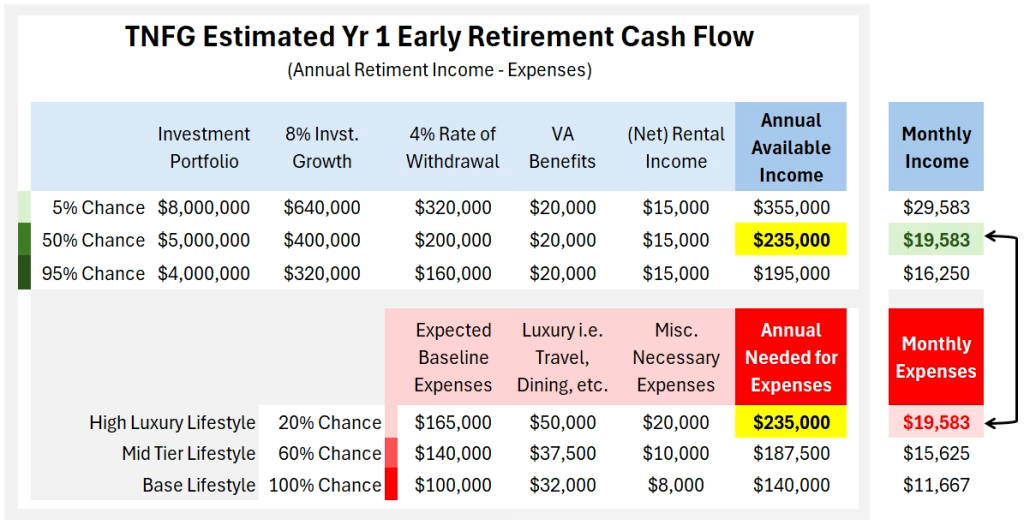

For our household, we have an initial BIG three that morphs into five income sources, minus any additional shenanigans we get into. Specifically for year 1, we use cash savings and will keep an eye on the market. No need to take money out during a downturn (learn more about Sequence of Returns Risk). After that, we will be living off my VA benefits, Investment Withdrawals (or Dividends), and some rental income (see Exhibit B).

It also helps that we are retiring with no debt. No massive monthly expenses, i.e., mortgage, unless we want to.

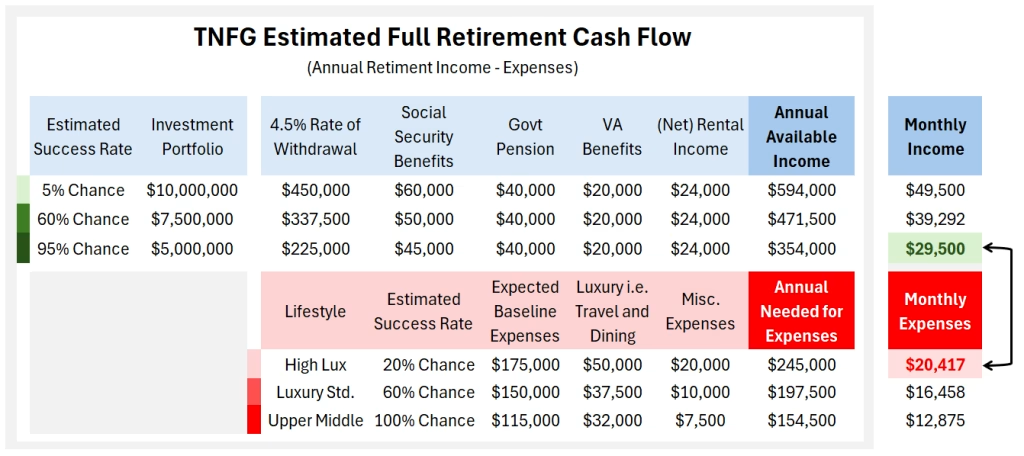

Around year 10-15, we phase in my government pension and social security (adding an extra $100k). Additionally, we will have to withdraw more money since the IRS wants that minimum distribution cut (see Exhibit C).

Required Minimum Distributions (RMDs) are mandatory annual withdrawals from traditional IRAs, 401(k)s, and similar tax-deferred accounts, starting at age 73 (rising to 75 in 2033) (learn more about RMDs). With all that said and done, we are looking at a monthly income of north of $25,000. It’s way more than we can consciously spend.

While we do plan to be philanthropic, we will be leaving a hefty sum to some fortunate heirs and such. Who knows, maybe they end up blowing through millions; either way, I’d be long gone. I never set out to spend like a fake celebrity; I want to travel the world, eat well, and do good. The financial stuff is just a mental exercise for me.

There is a 95% chance that we pull in $29,500 monthly while living overseas with 100% monthly expenses of less than $15,000. It would still be a great life. So is it better to keep working beyond 50? The answer is a resounding ‘No’ for us. We will be busy doing other things in retirement.

Conclusion – Early Exits and Way More Fun

In the end, I love the odds. Call it ego, but I’m confident in the math.

Besides, it’s just a plan. Plans are flawed, and they will likely fail, yet with equal opportunity to reach a desired destination. For example, you plan to get groceries. Some items are there. Others aren’t. And yet by the end of the day, you still purchased groceries.

There is a lesson in there if you squint. I don’t want to spend the rest of my time dreading Mondays and going through pointless performance evaluations.

About Author

{kind=link}