How to Make the Most of Money When the March Market Take Hits

March investment madness finally concluded. The S&P 500, the most appropriate benchmark to track, fell 4.6 percent for the first quarter of 2026.

The big lesson— nothing stays the same. You have to stay on your toes for this one. Your cash flow management is essential. Q2 promises even more of the same. It’s getting expensive out here, plus taxes, tips, and parking fees. Eating out (+40% over cooking your own food) is now an activity for the wealthy or the financially foolish. In the District of Columbia (DC), expect to pay 10% sales tax with a minimum 20% tip. At higher-tier restaurants, expect a mandatory gratuity fee. Brace yourself for a bumpy 3-4 months, as gas prices escalate.

Now more than ever, you need to double down on financial literacy. It’s mandatory. By definition, Net Worth (otherwise known as wealth) is equal to the value of what you own (Assets) minus what you owe (Liabilities).

The last time the market went down in 2020, some Americans rode the wave back up to million-dollar status. From budgeting to investing, the estimated median household wealth increased by 60 percent since 2022. If your net worth was $250,000, your household should have climbed to $400,000. Are you doing the work to build wealth, or complaining about fairness on social media? The world is changing, and it’s not going to be cheaper.

When prices won’t go down, the next best thing is to 1. draft a 5-10-20 year plan, 2. cut back on spending, 3. increase your income (where possible), 4. decrease your use of credit, and 5. Invest for the long term. Unfortunately, most households are not doing any of these steps, and it shows.

Table of Contents

March Inflation and a New Conflict

This March welcomed the Chaos Market

In 2025, the net worth of households increased by $5.85 trillion. Americans’ equity holdings rose by $9.29 trillion, while real estate assets grew by 990 billion. Although the first quarter of 2026 was fraught with economic, geopolitical, and market turbulence, Americans aren’t doing as badly as the media suggests. Slowing economic data, rising global tensions, and increasing policy uncertainty contributed to increased market volatility and U.S. equity market corrections. The uncertainty of war kept the Federal Reserve on the sidelines.

Household total debt balances grew by $56 billion in 2025. This brings the total to $19.95 trillion. Of which, mortgage balances increased by $1.16 trillion, reaching $13.77 trillion. It accounts for 69% of overall household debt. Consumer credit debt grew by $15 billion.

The financial situation is precarious. The worst may still come with hopes of relief by mid July 2026 if things cool off in the Middle East. And also if Trump decides not to do anything about Greenland or Cuba.

All about Inflation Madness and the Cost-of-Living Crisis Pot of Gold

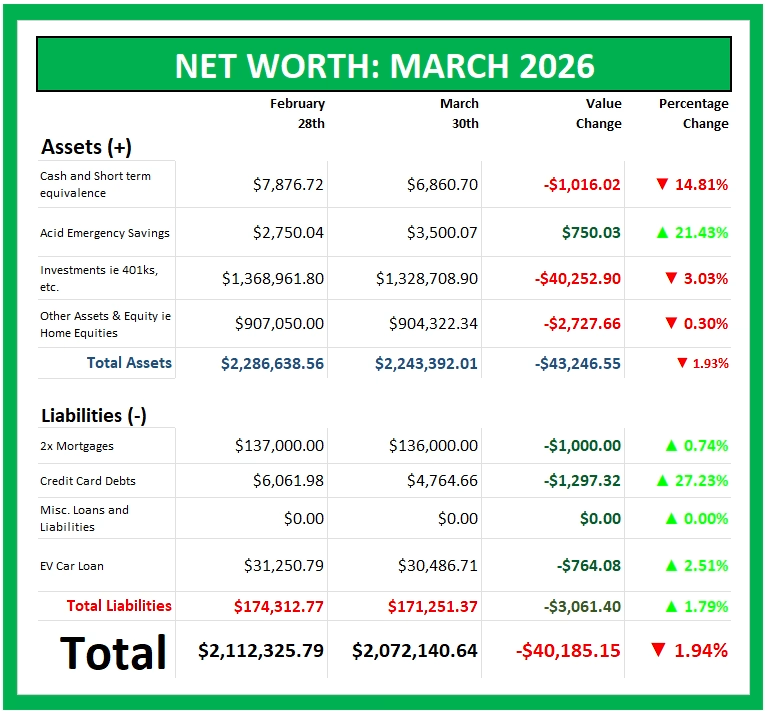

This is our TNFG monthly Net Worth Breakdown for March 2026.

Every month, we share our numbers to see if we can make cents for all the nonsense. Additionally, I drop gold nuggets and hints to improve your financial understanding. The goal of sharing monthly is to disprove others; It’s not impossible to grow wealthy. Building wealth works, even when the world seems dire.

In the end, consistency matters, so put in the time. You will find that the journey is one of self-discovery and change. It’s not the money at the end of the rainbow; you will come to realize that it was always about your time. Furthermore, try not to get too hung up on situations that you have no control over.

March 2026 – Gas is Up, Everything else is down

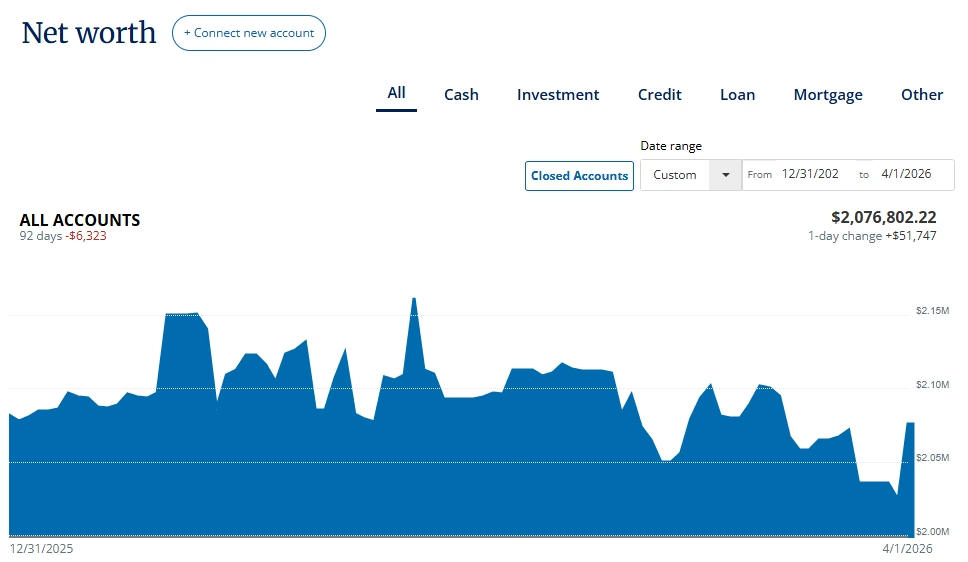

Our next household financial goal is to hit $2M Net Worth back in September 2025. Even with the hits, we managed to stay after that line through Q1 2026. We are still punching above our weight class and fighting the travel costs of 2025. Even with unanticipated costs, we managed to keep our cash flow average above $2,250 for Q1. If we can keep up this pace, 2027 will be the year when we move from paycheck to paycheck.

With our plans set for retirement at the end of 2032, we have to clear our credit card debt by July 2026. Our travel costs for last year were estimated way too low. Two weeks in Switzerland (+Portugal) and Brazil clocked in nearly $15,000, respectively. We have a better grasp on it this year for Mexico and Peru (+Colombia). Prices aren’t just up domestically; inflation is global.

Like a lot of Americans, we are feeling squeezed. However, unlike others, we know that any financial crisis comes in waves. It’s best to prepare and stay the course.

See our ending Net Worth as of March 31, 2026 (below)

Investments caved in due to More Trump Shenanigans

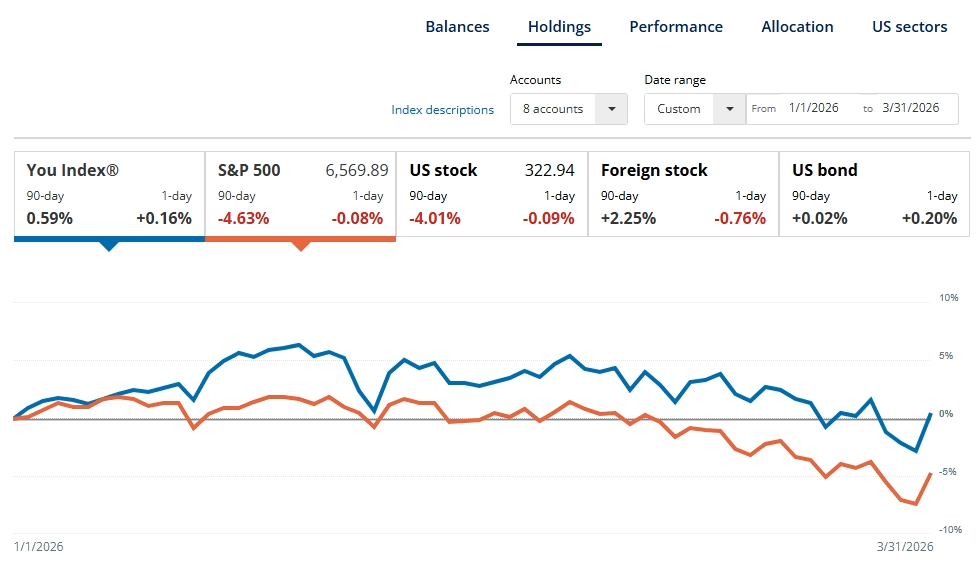

Wall Street ended the quarter worse than I thought. Investors panicked, which drove stocks down in the first quarter of 2026. The Dow Jones Industrial Average fell 3.58 percent, the S&P 500 slipped 4.63 percent, and the Nasdaq Composite tumbled 7.11 percent.

Our portfolio is down 0.59 percent for the quarter. Yet, it’s still way too early to cry. It can get worse. At this rate, I don’t anticipate a rebound until Q3. This might be a 2022 down year. The needle is pointing at -3 percent to -8 percent; time will tell.

Damn, the market is Decent in the Final Minutes

Sometimes the finish line is better than the race. Our first goal was to knock down credit card debt. We dropped it by $1.3k.

Mrs. picked up a higher-paying job with more stress. Time will tell if she holds out.

We are clawing back our savings from now to 2032, with an end goal of $150,000. For now, we are adding $750 monthly and will pause at $12,500. Instead of being fearful of consumer debt, we are opting for an active cash flow management approach. This includes a robust Acid Emergency strategy.

In the end, our wealth dropped by -1.94% (a dollar value of $40,185.15).

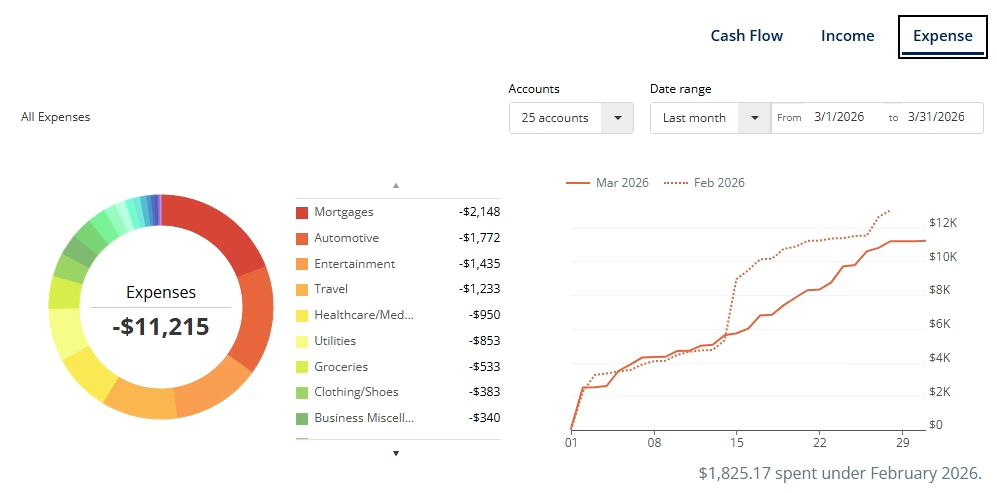

Our Household Expenses for March 2026

Aiming for +2k cash flow

One massive drag is the $1,500+ monthly payment for the new car, gas, and the associated car insurance. Can’t wait until we clear that hurdle at year’s end, 2027. While not massive in March, travel purchases are coming in for Mexico and family visiting.

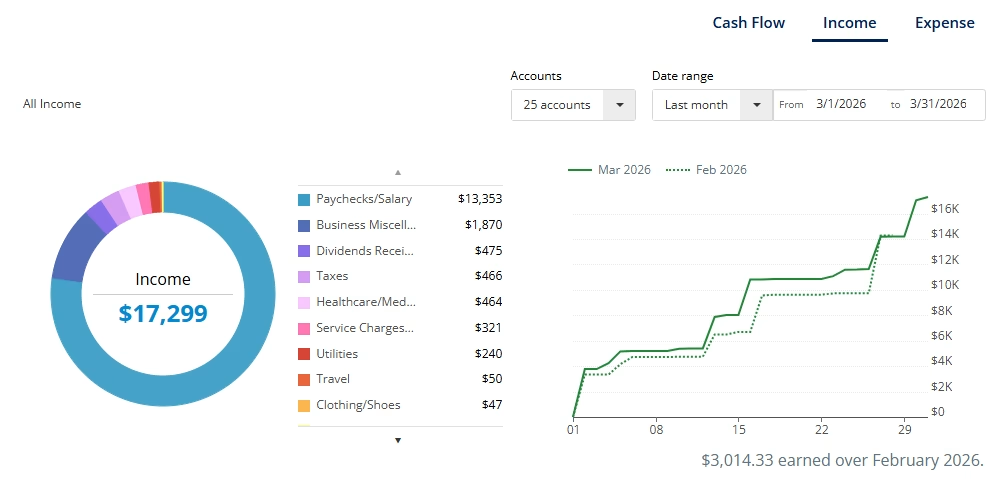

Income was robust for the month. The after-tax version always hurts the soul. It’s all about the net version. With the income at $17.3k and the expenses at $11.2k, we were left with enough money to move around.

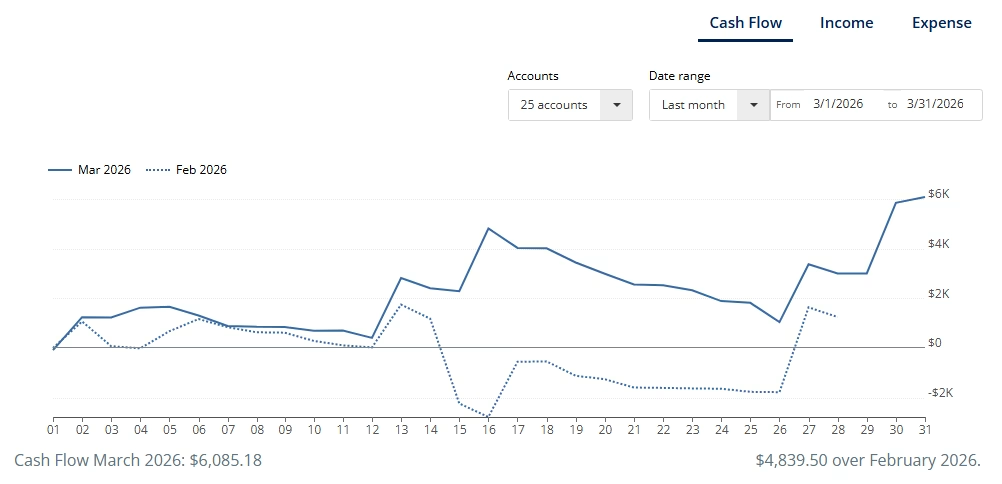

Cash flow management is the key to building wealth effectively.

While I see a lot of people pushing the Debt Free Journey or the FIRE movement, I’m just sitting on the side with the Net Max Financial plan and doing both. Why? Because that’s the opportunity that an effective cash flow management strategy offers. Either way, check out our full cash flow for March (below).

Beating March Madness, Looking Toward the Intersection of Money and Trumpflation

Although we didn’t beat the buzzer, we got each other. I really couldn’t do this journey alone.

Beyond that, here are our overarching goals for 2026:

- Back-load our ROTH IRAs to invest in the Sinister Six. Adding to our long-term strategy to retire early with north of $3M.

- Investing $250 per month in M1 Finance Brokerage focused on Growth and Dividend Income that generates at least $1,000 in passive income in 2026.

- Check out the portfolio in real-time.

- If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate with the push for a $2,500,000 net worth.

- To help monitor your savings, cash flow, net worth, investments, and retirement, use the Empower App (formerly “Personal Capital”). Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

- Prepare for an Epic Financial Literacy Month: (2) Workshops, (2) Podcast Interviews, and (4) Blog Posts. Pushing to build a $1,500,000 investment portfolio.

- Reading and Traveling

About Author

{kind=link}