How to Stay on Track to Reach Early Retirement

Every couple of months, we receive comments and inquiries about how feasible our retirement goals are. Most of these inquiries are side-eyes from Whole Life Insurance (IUL) sellers, but hey, they are still inquiries. Some concerns come from “social media financial advisors.” I have to air-quote that because no one knows if they are truly certified financial advisors or if they are competent and qualified. Can’t trust everything or everyone you see on social media. With that said, I can give them a pass.

However, I’m not posting on social media through copy and pasting Dave Ramsey, Ramit Sethi, or the guy who wrote the Simple Path to Wealth. The link is proof that I’m not a hater; I’m not much of a blind follower. I’m really this beastly in real life. I’m a rare confluence of bad circumstances and challenges. My parents all but abandoned me (at eleven months), which led me to a chalkboard learning math from my pre-engineering Aunt in Port-Au-Prince, Haiti. Come to think of it, she might have been in her first year of college.

Suffice to say, she was a math wiz. After a bunch of focus exercises (i.e., stick or belt), she placed me on the path to be a math wiz, too. While I’m not sure about her motivations, she taught me one important concept, “fè lojik la [Haitian Creole].”

The rough Haitian Creole translation is “Do the logic.” It’s one of the most brilliant lessons that I ever learned, and the simplest.

Table of Contents

The logic behind the Wealth Math

In Haiti, education is not free. You have to pay for it, and money isn’t cheap. As such, my corrections were mandatory to ensure survival. The classes were brutal with zero time for horseplay.

Any course of study, i.e. book, would be taught from cover to cover. The tempo never slowed, and if we got through with the content, then we moved on to the next level. If the students didn’t catch on, it was either their fault, the parents’, or maybe the teacher’s. The latter likely needed to be more brutal with the full support of the parents. The school was a pyramid of knowledge. Since the school ranged in ages from seven through eighteen, we literally looked up to the upperclassmen. Basically, it was pretty epic.

My aunt’s lesson on logic was critical. Unlike the U.S. Educational schema, there were no multiple-choice answers. The guesswork was thrown out completely. You either know the answer or you don’t. It was possible to gain some points if you knew the path to arrive at the solution. So at the age of seven, I had to know the solution to an algebraic equation, or a bit of correction was on the way.

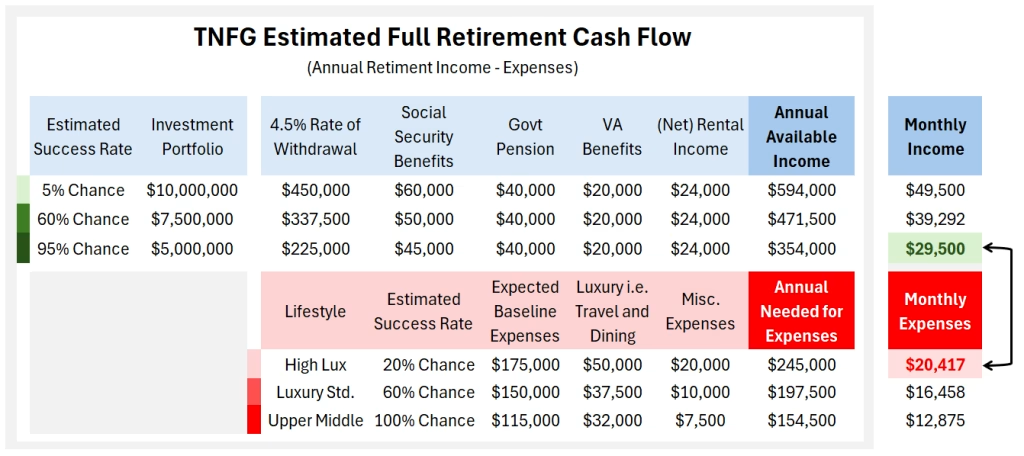

Because of this, when I say we will reach early retirement with +$5 million net worth, ‘Je suis sur et certain [French].” The math is not as difficult if you have a solid financial plan (check out the Net Max Financial plans). After reaching $2 million in net worth in 2025, the rest is a function of time. All the corrections also taught me to show my work (this website).

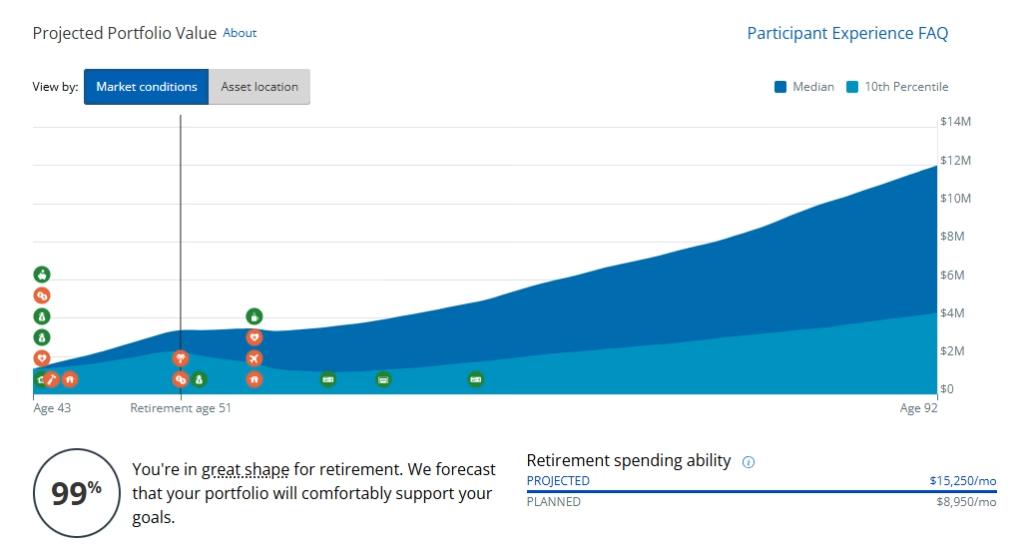

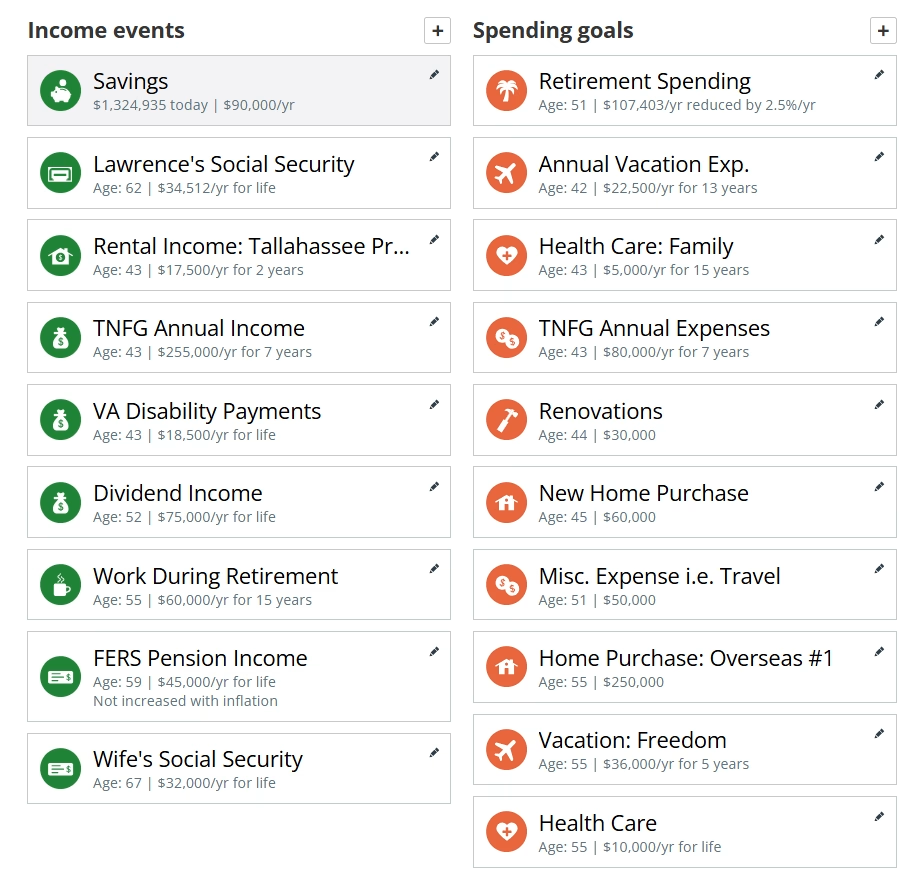

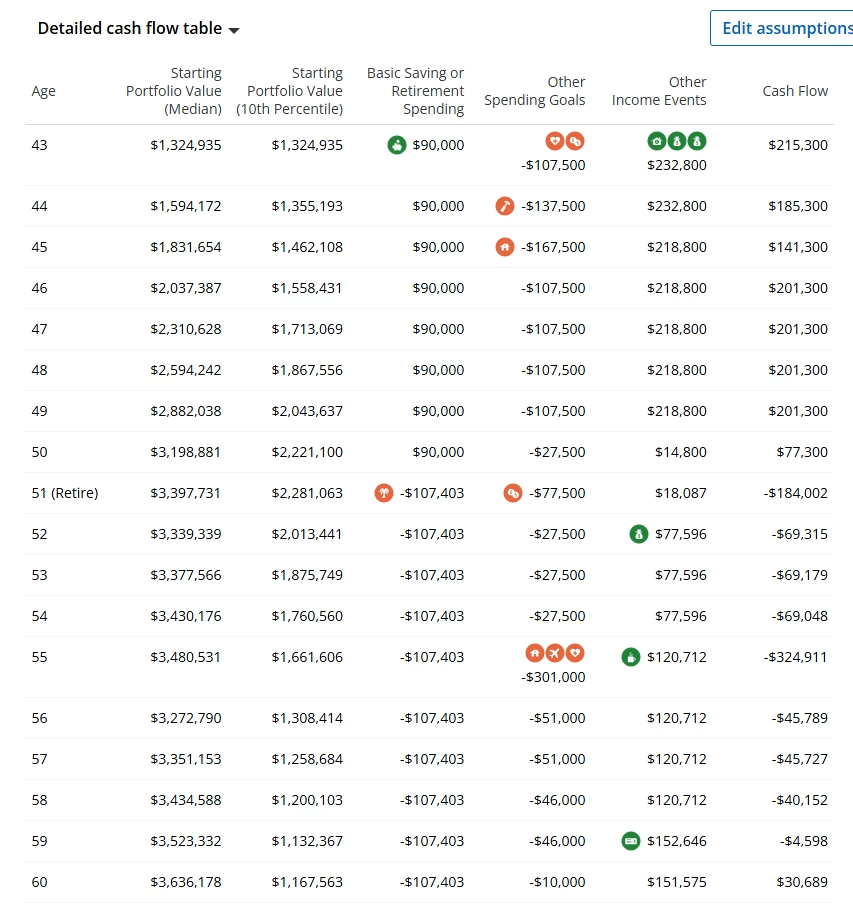

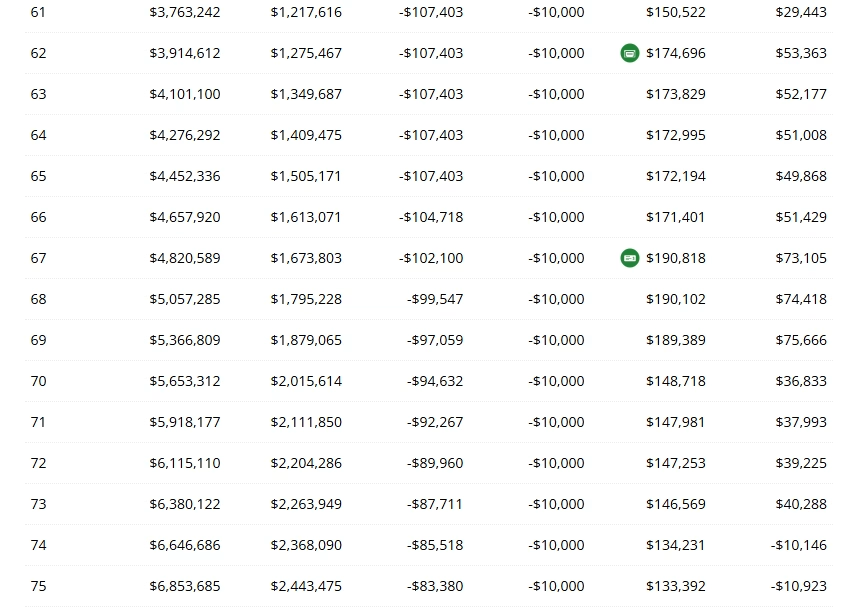

Retirement Projection through the Empower Website

Fortunately for me, on the Empower website formally known as Personal Capital, I can pull up a mock Monte Carlo simulation. For those who don’t know, here’s a short blurb if you never heard the term before.

“Monte Carlo simulation is a computerized mathematical technique that models the probability of various outcomes in processes with high uncertainty or many random variables. By running thousands of simulations using random sampling, it predicts the likelihood of different results, often used in finance for risk analysis and engineering for complex systems.”

This is basically what financial planners use when they turn the computer away from you. If you want to save some coins, use the website.

A couple of notes here: the website’s (low estimate, i.e., 8%) total investment portfolio, not total net worth. It doesn’t account for big shifts and increases. Yet this is still a great tool for where we are headed. This is subsequently how you stay on track to reach early retirement. You have to double-check the math.

With that said, nothing is clairevoyant and FREE is FREE. The tool is just an opportunity to go over your work and ensure you are on the right path. Check out the data with notes below on my household’s early retirement plan:

About Author

You May Also Like

Are You Really Rich or Just Playing Expensive Dress-Up?

TNFG Weekly Chapter 8.5: Healing Broken Financial Relationships

{kind=link}