All’s Fair in Love, Tariffs, Stagflation and War

All is Fair in love, stagnation, and War. Should we have even been surprised by February? January has the sell-off for profits and tax planning, while February folks take profits.

What started with a tech slump ended with Nvidia leading the way with its 12th earnings win, followed by a prompt sell-off. Crypto bros are having a harder time with Bitcoin (BTC) dropping to $63,000. BTC is down over 20% year-to-date. Being down as much as 40% for the last 6 months has got to hurt.

Stock markets are plummeting like the economy. The Trump 2.0 house of cards has gotten expensive and time-consuming for all Americans. In 2024, we were warned about the tariffs. By now, China has emerged as the big winner, on the heels of the US Supreme Court ruling against the tariffs (February 20, 2026). Ever since Trump got into office, it’s been one battle after the next. Well, at least the price of eggs is down. Oh, some companies are suing Trump, which means we are getting sued over the tariff shenanigans.

Inflation is sticking around like an STD. Inflation decelerated in January. Price pressures eased across some consumer staples such as food and gasoline. Other categories remain elevated, like electricity and home heating, economists said. With those headwinds fading, we should all be worried about overheating in 2026. The global risk is stagflation.

Table of Contents

Here’s a refresher on inflation and Stagflation

Inflation is a universal constant. It’s not a novel idea. When prices spike, people panic, and the media covers it for views. Fear sells and generates a lot of ad revenue. However, fear is fertile ground for misinformation.

Beyond the clicks and ill-informed conversations, the problem remains. The problem is over-expenditure. The solution is to SPEND LESS. There is no way around it. “Too many dollars chasing too few goods,” which means everything will cost a lot more, for a longer time, because demand outweighs supply.

Secondly, inflation may slow down, but it isn’t disinflation. That means prices won’t miraculously go down.

For example, if your Amazon purchase cost $100 in 2020, it went up 9% in 2021, 5% in 2022, 3% in 2023, 2.5% in 2024, and 2025, respectively. The new price is $117.88.

Even if inflation goes down to 3% in 2026, the new price is $120.13. You are looking at a 20% increase.

Aside from drastic austerity measures, the only thing that cuts prices in a good way is bold innovation and investment into tech.

Inflation means that your current annual expenses in 2026 of $85,000 will cost as much as $170,000 by 2050. Why? Because humans operate on limited resources. The fewer items we have, the more people want them; the more expensive it becomes.

Additionally, spending and access are now global. The emerging middle classes in India, China, and South America will want access to the same goods that Americans had for the last 50 years. Translation: get used to the new prices, and years from now, they will be the low prices. All of this is better than Stagflation = high inflation, stagnant growth, and higher-than-average unemployment.

The average American household will need to become more mindful of its cash flow.

With all that economic pillow talk aside, time to get back into the Financial Driver’s Seat

Welcome back to the TNFG’s monthly breakdown, where I dish out all the secrets on the way to becoming a millionaire household in this lifetime. Disclaimer: Like all married men, I have to get approval from the Mrs to say, write, and do anything. And even then, my actions can be repealed or sanctioned.

On a personal note, this month was harsh. The winter storm was brutal, and the news was wild. Societal burnout is setting in. Be careful in your day-to-day commute; there was even a mass stabbing on the highway.

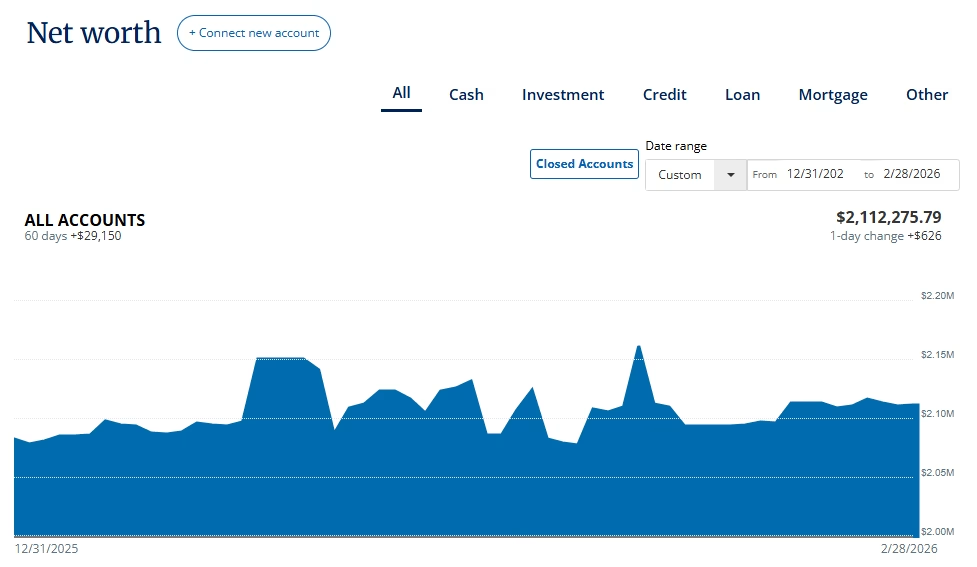

Our net worth goal was $2.5 million (by December 2026). Quarter 1 and Quarter 2 will be tumultuous at best. Every time the Trump 2.0 administration does something, markets move. Stay on your toes.

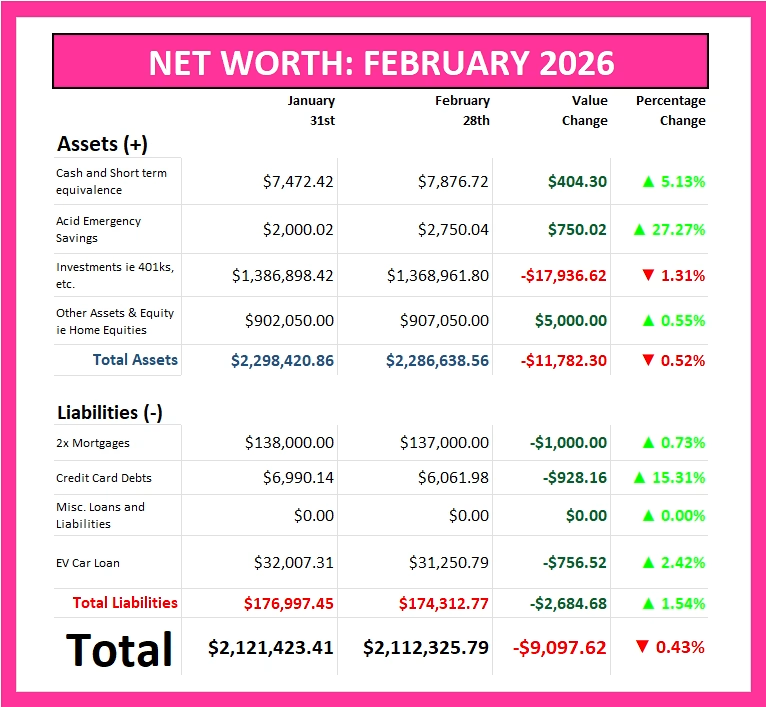

Here’s our Monthly Net Worth Summary:

More Market Swings with More Turbulence Scheduled

We are back in the K-shaped Cocaine Bear economy. Keep your hands inside the ride, extreme highs and lows, as the wealth gap in America increases. The future belongs to long-term investors. There are no shortcuts, and avoid FOMO. Try not to panic sell, especially as the new Middle East conflict escalates. You already lost the paper gains, no need to lock in real losses.

At this stage, it is best to plan for the future and continue long-term investing while the market continues these violent up-and-down mood swings. Costs are only slated to rise by 2040. The only hedge against that is investing for the long term.

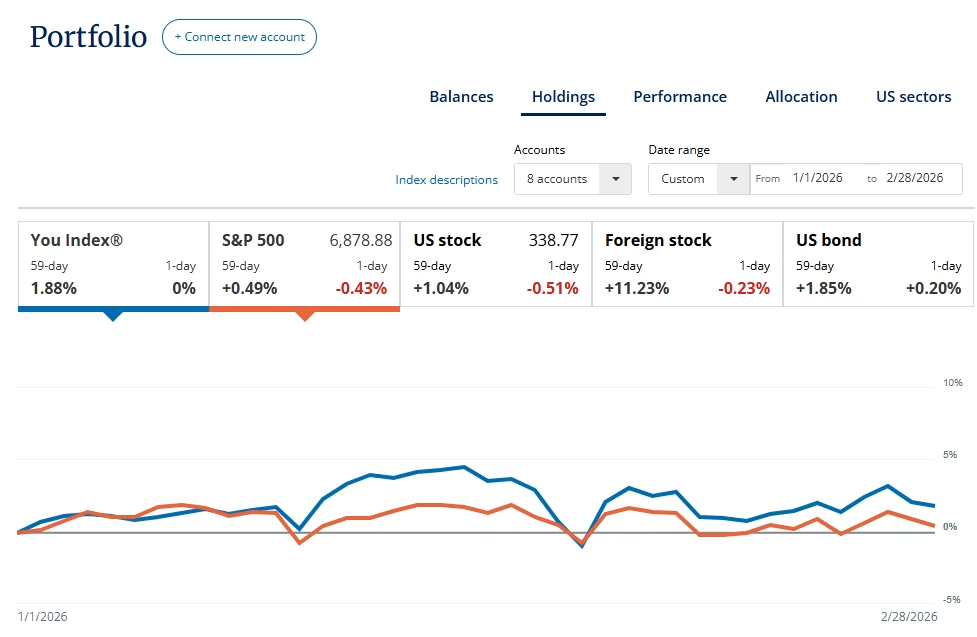

Overall, our investment portfolio dropped by 1.31%. We are sticking it in our net max financial plan and betting on the next 5.5 years til we retire. Fortunately, we got active and purchased more Health and Energy stocks while the market retreated for a few weeks. Also shifted the main 401k to receive more international exposure. You have to be proactive and engaged in this game.

When we get within five years of our retirement goal (2033), I might change some of our strategies. Check out our Google Sheet.

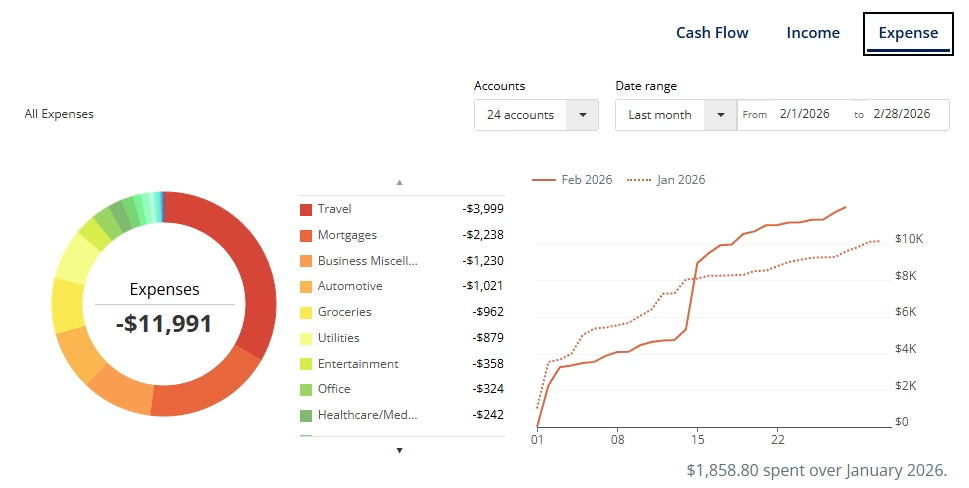

Spending a bit too much on everything

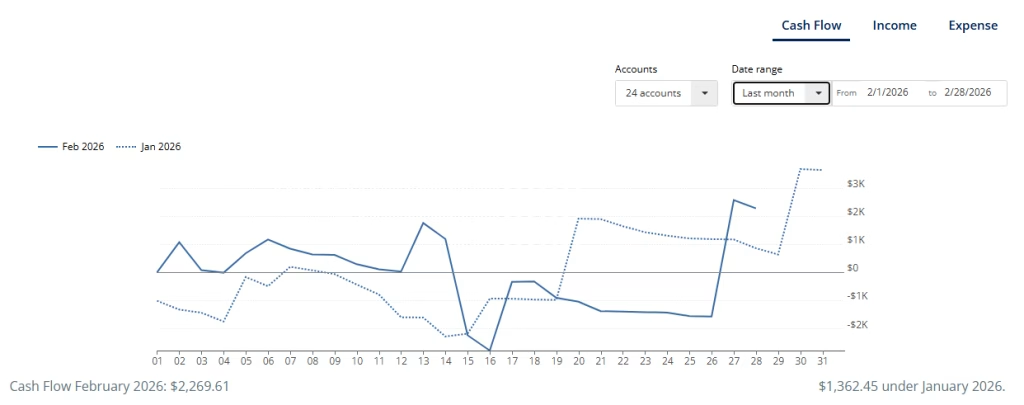

With prices up on just about everything, we didn’t love our February spending, but we offset the cost with our income. Our net cash flow was +$2,269.61, an increase of $907.16 over January 2026.

Part of that was due to our travel costs being front-loaded for Mexico (see “Budgeting” below). Well, all travel is expensive in 2026. We pushed Japan purchases until mid-March.

We are doing a lot better with our Amazon purchases. Additionally, we cut down on unnecessary subscriptions last year. We are way more focused on gym/family time. Mrs. TNFG started a new job, so it’s going to take time for us to adjust. I’m going to try to get more quality sleep.

Getting used to a new schedule of reading, gym, and longer commutes.

As for Love and Wealth, What is the Next Step for Us?

Since our love language includes retiring early and traveling the world, here are our overarching goals this year:

- Add more date nights at the Mrs.’s request. No point having perfect credit, solid net worth, and decent emergency savings if we aren’t looking at our mental health and connecting on a personal level.

- Even though financial resources are low, investing at least $833.33 per month in M1 Finance Brokerage focused on Growth and Dividend Income that generates at least $1,500 per month in passive income in 2033, is still the goal.

- Check out the portfolio in real-time. If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate of $7,500 per month.

- To help monitor your savings, cash flow, net worth, investments, and retirement with Empower.

- Hit 17,500 followers on Instagram.

About Author

You May Also Like

How a Great Budgeting Plan Can Help You Live Off of $112,000 Per Year for the Rest of your life

The U.S. Kicked Off the New Year with $1 Trillion in Gains!

{kind=link}