How to Financially Survive Trump’s Latest Spring Fling

While most people don’t agree with this self-inflicted war for oil, April was a reminder that Trump’s latest spring fling was great for investors. Try not to get cute with holding too much cash. It’s getting more expensive for longer. Fuels up and buns out for summer.

Buckle up during this 250th U.S. birthday because it will be a rollercoaster through Q4 2026. If that’s not enough, Tipflation isn’t taking any prisoners. In Washington, D.C., we are paying 10 percent on sales tax and 20 percent on tips. We are 30 percent deep before you even take a bite or enjoy the experience. It’s best to stay home for a bit if you can.

The Federal Reserve met on April 29, 2026. It marks the last entry in Jerome Powell’s tenure. The leading officials decided to keep interest rates steady at a range of 3.5-3.75 percent. While the media decry the 8-4 split vote decision as significant, it wasn’t. We are in a precarious time. By the end of the year, they will realize that we needed to raise rates at least one time to push consumer spending lower.

This is the ‘not normal, new normal‘. Americans are entering the Struggle Era as the reversion to the global mean puts downward pressure on once-subsidized lifestyles. What does it all mean for you?

Similar to last year, here’s how it will affect each group:

- Spenders – not good. Every dollar matters; the more you spend, the deeper the hole you are burying yourself in.

- Savers – meh. Higher-than-average interest rates translate to money being printed monthly or quarterly. But it won’t outpace equities.

- Investors – pretty good. Market fluctuation and turbulence aside, if quality companies are dropping sub-10 percent, the correction might be a great opportunity to bank on future returns.

- Near-retirees or retirees – not good, but it depends on your cash flow. You might want to stay on the job for an extra year. Boomers need to get a will on paper because the clock is ticking. Funerals cost north of $20k nowadays.

Table of Contents

A Better Financial Plan Pre-, During, and Post-Recession

My wife and I hit the $1 Million+ Net Worth in August 2023. We were featured on Bankrate’s “How Black families can build generational wealth, according to experts.” Now we are setting our sights on the $2M mark. With these headwinds, we will lock it in for 2026.

To think that as of April 2020, we were hovering north of $220,000 following the COVID crash. This is wild proof that sticking with it works over time. No matter what’s going on, there is always room for improvement and wealth building. IT WAS NOT EASY. However, the journey was made easier by not over-leveraging before the pandemic, way back in 2012.

If you are new here, this article is the TNFG monthly Net Worth Breakdown for April 2026. You are in the right place to see if we can ‘make money, make sense’. Additionally, there are always usable financial nuggets that might help you along the way. Our goal is to show you what we did so that you can do it better.

The best way to survive the next recession is with a great financial plan.

Can We Do This Recession Already?!

I like how MarketWatch puts it: “Don’t worry about the recession coming, it’s likely already here.“

The probability of a recession is up in the air. It’s always been that way and will always be that way. Why?

Recessions are cyclical. Basically it happens all the time.

It’s like worrying about the night coming at the end of the day. It’s part of the fabric of how human beings interact with more. I think of it as a recalibration of wealth and an opportunity for the next generation to jump in. Instead of growing in fear, lean into learning. Accept challenges and become more resourceful.

I started digging into the pantry. Maybe it will help lessen my big back. This is a great time to become better cooks. As restaurant prices skyrocket, cooking is a premium skill. We paid $150 for four drinks and two appetizers. DC prices are increasing on top of the 10 percent sales tax and the near-mandatory tipping of 22 percent or more. I was about to purchase a half chicken combo from Nando’s. With the prospect of paying $25 total price for mid-meal, I reminded myself that there is food at home.

God bless his soul, cause I’m not going out anymore. There is no incentive when there is food and drinks at home.

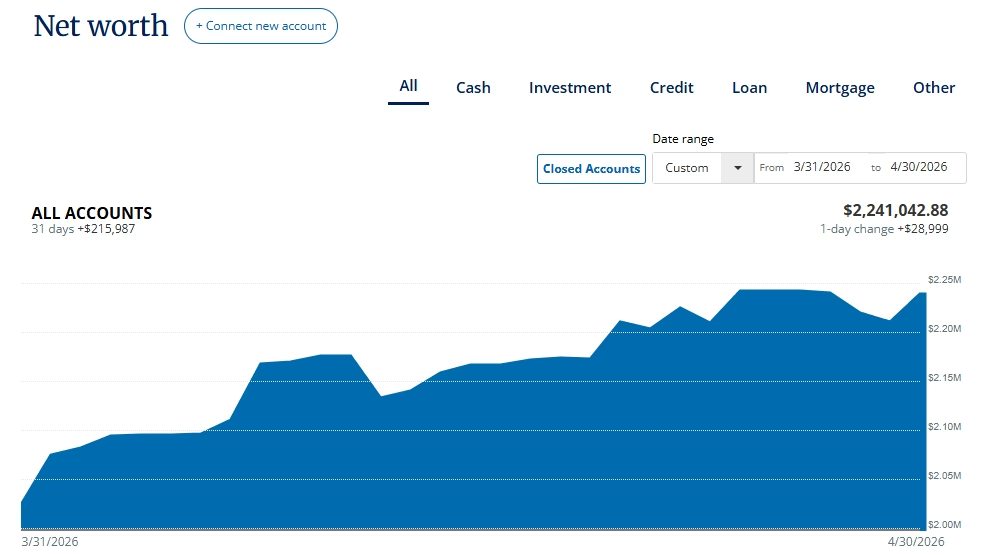

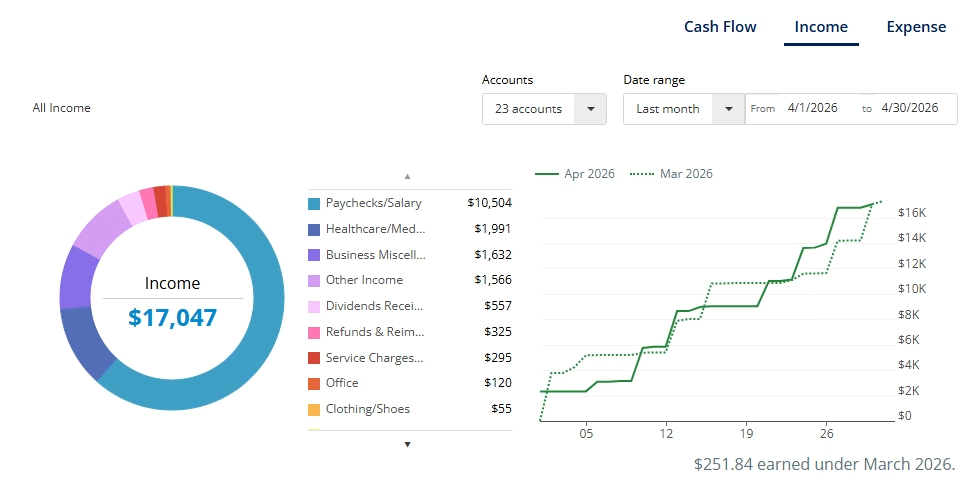

Our Net Worth Rebounded post Q1 with $216k!

Lesson – Stocks will drop by 10, 20, or even 40%. Try not to lock in the losses.

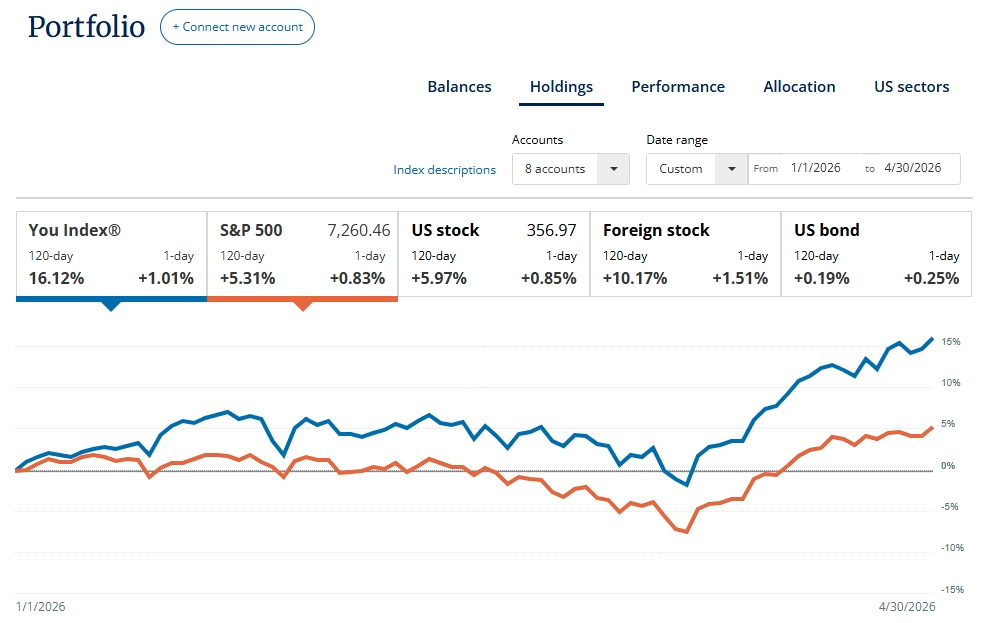

The month was chaotic but good. April brought the sunshine and a green reversion. Investors made up for the losses in February and March while picking up a bit of steam for the rest of the year. We all but shrugged off the Iran issue. The market clawed back and said no more Bears (for now). The big winners are those with the nerve to buy the dip. See screenshot #2

What’s the current strategy?

Absolutely nothing.

When things are chaotic, the best you can do is to hunker down as tightly. Pay off what you can and keep going with your financial plan.

My wife and I intend to pay down our credit card debts by July. After that, we need to raise our savings to $35,000 (per Investopedia) through 2028.

While stocks are cheaper, we are locking in purchases of Amazon $AMZN, Eli Lilly $LLY, Sandisk $SNDK, Western Digital $WDC, and some energy. These are quality stocks to buy and hold for the long term for our portfolio.

Our goal is to rebalance into some consumer staples and healthcare. The latter sector is down as much as 7% for the year. Might be a good buying opportunity. I’ll keep an eye out for dividends through Realty Income $O.

In the end, try to avoid the urge to spend and increase lifestyle expenditures. This is the time to build your savings and purchase stocks. This strategy is a hedge for the future. Those who adapt will win.

What Happens Next!

The post-Trump 2.0 is different. It will be a while before we feel a sense of ease. There is still a rise in mental health issues that we will all have to contend with. Additionally, there is a growing sense of entitlement for less effort. It’s best not to follow the crowd down the rabbit hole.

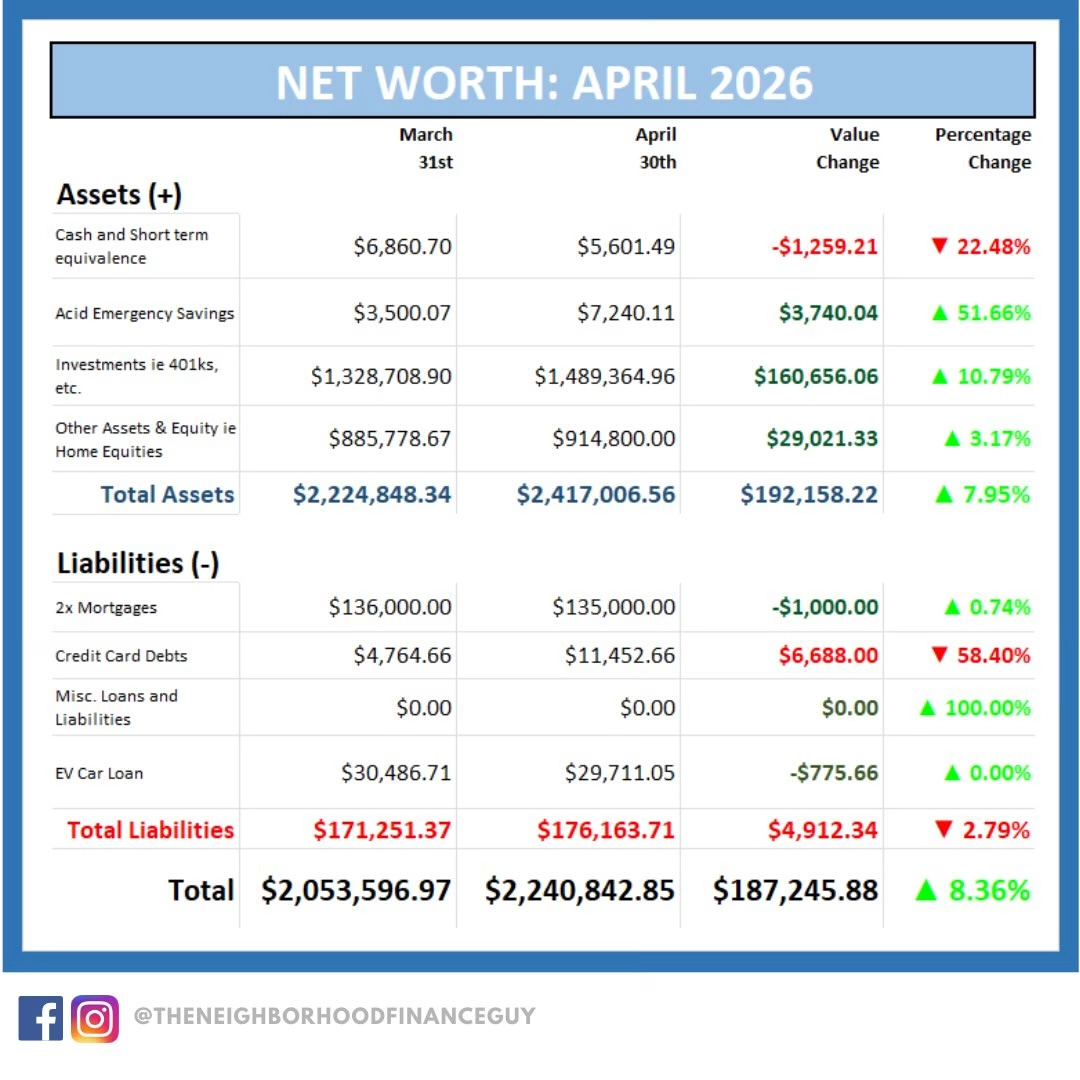

All things considered, our net worth is up 8.36 percent for the month. We readjusted our year-end goal to $2.6M (+/- $100k). The road to success is non-linear. It’s better to stay positive even during a negative month.

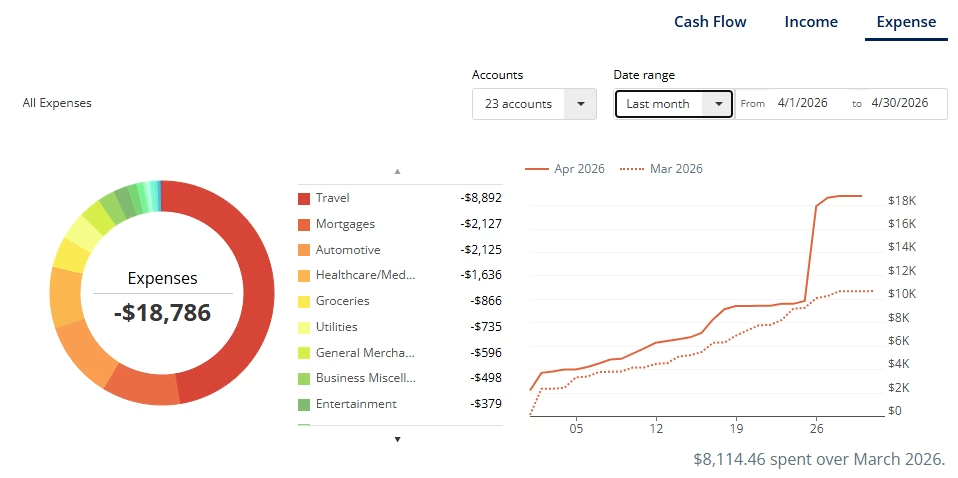

Financial Spring Cleaning Between High Expenses

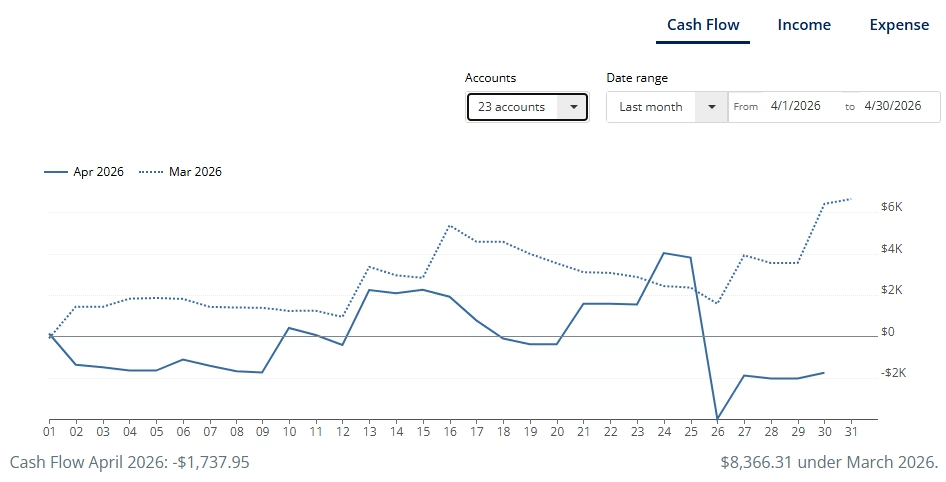

We locked in travel ($8.8k), definitely on the 4.5 stars level. I went on a travel clothing run through Amazon.

And we are tying up loose ends like Nintendo Switch 2 for entertainment and micro adjustments in the house.

Can’t forget about the $3k in state taxes due.

Inflation is a real thing. People are feeling it after all this time. I was warned about this in 2021. We spent almost $700 on food and restaurants. Our monthly amount in 2019 was, on average $600/month. This seems so long ago.

We’ve improved on our Amazon spending. Last I checked, we spent nearly $100,000 since 2012 on those deliveries. On average, each purchase was less than $35. This proves that it’s the death by a thousand cuts that gets you. Translation for me: Buy more Amazon stocks.

Avoided another expensive auto bill by doing the repairs myself

Luckily, we have two cars. One of them is an old and trusty 2009, while the other is a sexy 2023 car that all the robbers want. The monthly payments and insurance are roughly $1,000 monthly! And that’s every month. April is not beating allegations as our most expensive month.

Suffice it to say, it’s been a very long month. Right now, my mind is juggling how we stage our cash flow to start helping out our parents in 2027. After that, the next focus point is to retire by December 2032.

Money is getting tight, so we need to band together to make the dollars stretch.

Money stress breaks down people, relationships, and our bodies. It’s best to look ahead and prevent further wear and tear. There are a lot of home upgrades still pending. That’s how opportunities and choices come at you. You have to be five steps ahead to capitalize on the future.

You have to mitigate the future with mental preparation. We have to get that number back to $10,000 in our bank savings account by the end of the year. Our Acid Emergency Financial Plan helped us get through tougher financial times.

Time to reset.

Easing off Spending to Prepare for Whatever Comes Next

With prices peaking, it’s best to step back and not overspend where we can. Emergencies can pop up everywhere. We had a great talk about our goals and re-centered on how we would get there. Remember this key metric of wealth: “Stop equating happiness and social acceptance based on the money you spend.“

Beyond that, here are our overarching goals through 2026:

- Invest $81,000 for the year (which includes $10,000) in our M1 Finance Brokerages. Check out our Starter Kit x10 portfolio in real time. If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate with the push for a $5 million total investment portfolio by December 2032.

- To help monitor your savings, cash flow, net worth, investments, retirement, and more. All FREE with Personal Capital! Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

- Travel is set for 3 countries: Mexico, Peru, and Colombia. Pushed back Japan due to travel issues with the Middle East conflict. We prioritize adventures in our household. Secretly, it’s about the food and the sights. To do so, we leverage our travel credit cards for rewards and perks.

About Author

{kind=link}