The U.S. Kicked Off the New Year with $1 Trillion in Gains!

Kick-Off Season: Big Hits and Covert Operations in Venezuela

We started the year in our favorite location, Brazil. My wife noted that we’ve been in Brazil for four years straight, with next year being number 5. Why? We tend to take our anniversary trip at the end of the year, which then bleeds into the New Year. As such, we were in Rio for 2023-2024, then again for 2025-2026. We will be heading back for Carnival 2027. To be honest, I’m still reminiscing on these experiences.

Nothing tops Dinner for 2 for less than $50 versus the excess in Washington, DC for $150. The drinks are effective and never cheap, even if the price is less than $5. Sadly, the world is changing. Prices are high globally. Homes are still uniquely unaffordable. And stocks are tenuous at best. Consumer sentiment is holding on by a string.

Markets started 2026 with a solid, broad-based rally, as the S&P 500 gained 1.5%. We briefly surpassed the 7,000-point mark. Small-cap stocks outperformed, rising over 5%, driven by a rotation away from mega-cap tech into economically sensitive sectors. The Feds, aka the Federal Reserve, opted to hold interest rates. Inflation is proving to be sticky.

If the January Barometer theory holds, the year will be rocky for the first two quarters. The crux of the theory is that the investment performance of the S&P 500 in January predicts the year’s performance. Inversely, if they are lower in the first month, they’ll be lower for the year.

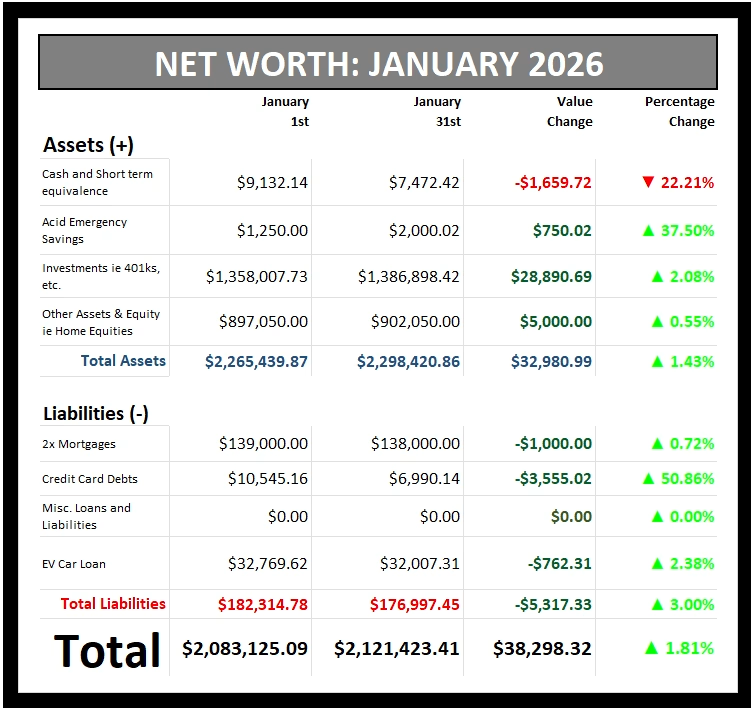

As such, the TNFG household came out on top. Our portfolio went up nearly +$30,000. This is still a better start than 2020, when we took our $50,000 tumble.

Table of Contents

Welcome Back! New Season, and More Information

Welcome back to a new year with TNFG’s monthly breakdowns. Our household’s 2023 Net Worth crossed the $1 million mark. We hit $2 million in September 2025, beating our January 2026 expectation. Now, we are aiming for a total investment portfolio of +$1.5 million by year-end (YE). We are nearly 5 years away from early retirement.

As of late January 2026, the S&P 500 reached a record market capitalization of $62.3 trillion, adding $1.2 trillion in value, driven by an AI-fueled rally and record-high trading volumes. Since this recap is posted in February, we lost all of that. 🤣

While it was uncomfortable, all Federal workers returned to the office in March 2025. This put a damper on our move to Orlando. With renewed vigor, now it’s all about living a balanced and healthy lifestyle on the way to traveling the world.

Mrs. TNFG picked up a new gig. A few more adjustments to our schedule, but nothing we can’t handle. No sad eyes here, as people are struggling to find employment. We are grateful for the chance and opt to do more with our time and dollars.

Just additional motivation to garner more assets, buy a forever home, and settle down in the DMV in 2027-2028. By all accounts, it’s not that bad since we have a light footprint, and we are flexible.

There is no progress without challenges. This is just one of them. We rest easy knowing that even if we don’t invest another dime, our investments will be worth $5 million by 2032. After that and some taxes, we will be traveling the world. We might even try to make a difference in the lives of others. I guess we will see when we get there.

Our Net Worth jumped, but we can’t get cocky too early

We remain very aggressive with our cash flow.

Because of that, we can maximize the yield of 90 percent of the dollars we earn. With our next goal of a $5 million portfolio by YE 2032, we will have to rebalance and reassess our investments as needed. Low performers have to go in favor of quality companies. On top of that, we will have to put $250,000 into our Acid Emergency Savings Plan.

It’s a lot to consider, but it’s doable. I recommend going bold with your ideas while keeping them feasible. After that, imagine what you need to do to make those big ideas work. It all starts with a financial plan.

When we started, we started at the bottom, too. That’s where all good stories start. Sharing the journey is important because we have never seen anyone who looks like us shift from the poor working class to millionaire status in one lifetime.

The US is still one of the few countries with an incredible upward mobility social class slope if you do it correctly. Building your Financial Intelligence through diligence and effort is the golden ticket.

Kick-Off Your Best Year with SMART+ER Objectives for the First 90 Days

Wealth comes down to three easy steps: 1. Decrease your expenses, 2. Increase your income and 3. Invest in the Difference. However, before you get there, create a 3-year vision and construct the plan. Be specific; the plan should have objectives and can be evaluated in 12-week intervals.

This will improve your life by 400%. If you aren’t addressing your smarter goals, you are merely working backward. Here are TNFG’s top three books to alter your life toward wealth.

Happy to See Our Net Worth Grow!

Our net worth went up 1.81% to $38,298 in cash value. There is always a bit of discrepancy between the last-day number and the first-day number, with slight fluctuations. Or there are late banking adjustments.

We were overweight in tech, and we got caught slipping. I’m hedging future investments with more healthcare and consumer staples throughout the year. Apple $APPLE and Google earnings came in mixed. AI fears are increasing. Buying stocks that had a bad 2025 seems to be working, like Bank of America and Exxon Mobil. I’m also seeing an optimistic look from the Financial sector, i.e., American Express, JP Morgan, etc.

Improving our cash-on-hand will be essential to capitalize on the price action going into the third quarter.

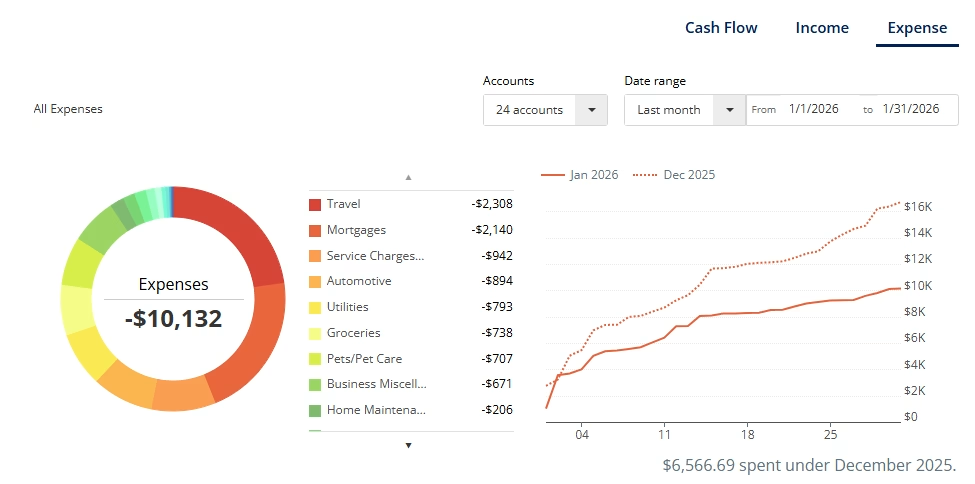

Travel, Groceries, Auto, and More Fees

My wife is always wondering, “When will we feel rich?” The answer is that we are rich together. But the real answer is, never! Just kidding. After that, she pouts again. Our 2026 household goal is to close out with $2,500,000 by December 2026 (+/-$50,000).

Beyond that, we have travels to plan for Mexico City and Japan. We are estimating at least $27,500 year, but at least it’s cheaper than the near $36,000 last year. It’s already $2k for the flights and an estimated $1.6k for lodging for the Mexico trip. It’s going to be great, but it’s not free. At least three domestic trips are being baked in as well. We haven’t even addressed the home renovations of over $30,000 (estimated). My wife needs a new bathroom to function. She is likely to throw out all my stuff.

There’s a lot of work to do. We are cutting down and strategizing. This is not a time to get cute; it’s a time to go lean and mean.

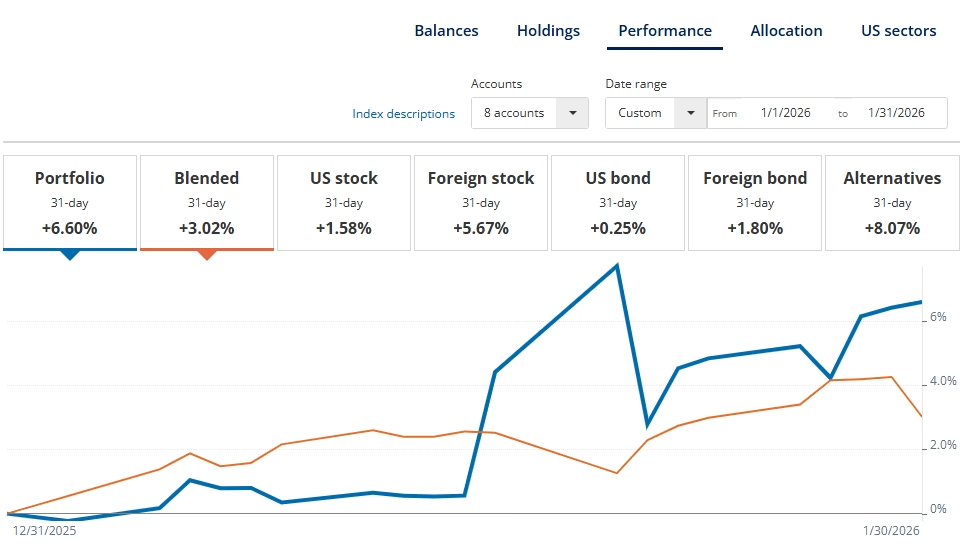

Our January Investment Performance Kick-Off and Fall-Back

Our investment went on a run in January and dropped off the cliff. We aren’t out of the fire just yet. We expect more corrections in Q1-Q2 2026. For now, we gotta restructure our investments. See the graph below. The price of long-term investments is subject to a rapid drop on any given day. One day, a negative $250,000 will be possible with a $5 million portfolio. You need to have the nerve to be wealthy.

Expect extreme volatility through 2027, with the Trump 2.0 administration. But I guess that it swings the opposite way to close out the year. As I stated before, this is an unequal economic recovery. However, if you aren’t investing today, you are compounding your issues for tomorrow.

This uneasy/perpetual struggle is what the majority of the world lives with. It’s not new. At this rate, Americans will have to learn to fight for every inch of a better life.

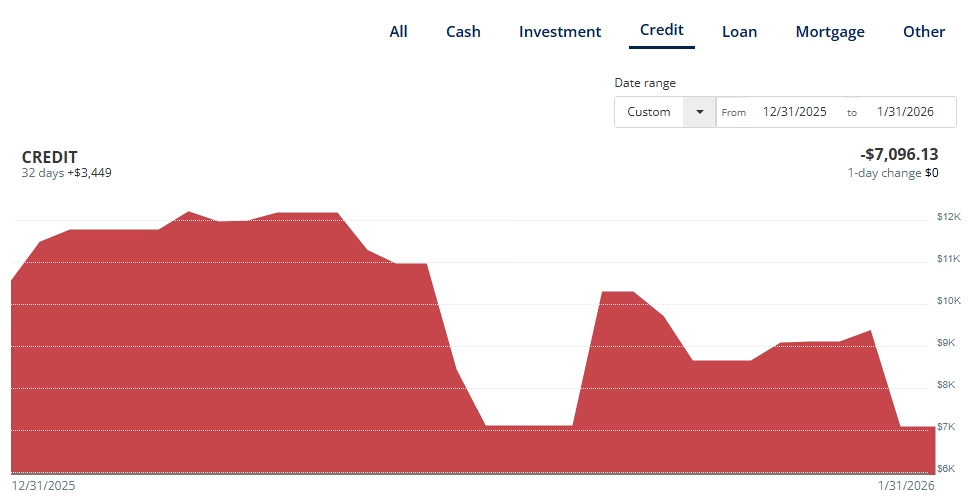

Savings Rates Stalling with Debt Climbing

Back in 2022, we opted to lower our interest fees by withdrawing $4,500 from our basic savings account (earning 0.01%) to pay off credit cards. We stalled out since. This year, we are building back our savings account to $7,500.

We will have to pay off debt the good old-fashioned way. One dollar at a time. Our goal is to keep investing since it earns our future while simultaneously keeping our interest fees as low as possible. Don’t sweat the increase since we have to buy the flights early. This might not have been the best kick-off for the year, but we are still happy, so it’s a joy.

How will TNFG Ride This Solid Kick-Off?

First, we have to look out for false stock positives. You can’t get too over-optimistic. Time to readjust away from low-performing stocks and stock up 10% dry powder for the next low. That’s our strategy moving forward.

Beyond that, we are paying down debts and investing:

- Even though financial resources are low, investing at least $1,000 per month in M1 Finance Brokerage focused on Growth and Dividend Income that generates at least $1,000 per month in passive income in 2027, is still the goal.

- Check out the portfolio in real-time. If you like the platform and want to start investing, I have the $10 for $10 referral if you need it – https://m1.finance/SYdqDJ2SyADC.

- Shooting for a sustained investment rate of $7,250 per month.

- To help monitor your savings, cash flow, net worth, investments, retirement, and finances with Personal Capital! Sign up with my link & get a $20 Amazon gift card. *Terms apply. https://pcap.rocks/lawrencegonz

- Hitting 15,000 followers on IG.

- Work on blog consistency while adding eBooks (at some point).

- Pushing to build out for the next year until we hit a $2,000,000 net worth as of January 2026.

About Author

{kind=link}